Report of the Cultivated Meat Investment Landscape in the Mid-Twenties

Point-in-time analysis (figures as of Q1 2025).

After a funding peak around 2021 and 2022, the sector experienced a downturn in 2023 (State of the Industry Report: Cultivated meat and seafood | GFI). With this report, I will analyse the market investment trends in 2025 compared to 2024, covering total funding volumes, who are the investors, what are the regional patterns, any deals and acquisitions, public market sentiment, and the challenges and opportunities behind these trends. I also want to assess whether 2025 has brought a resurgence in investment activity for cultivated meat.

Total Investment Volume in 2025 vs. 2024

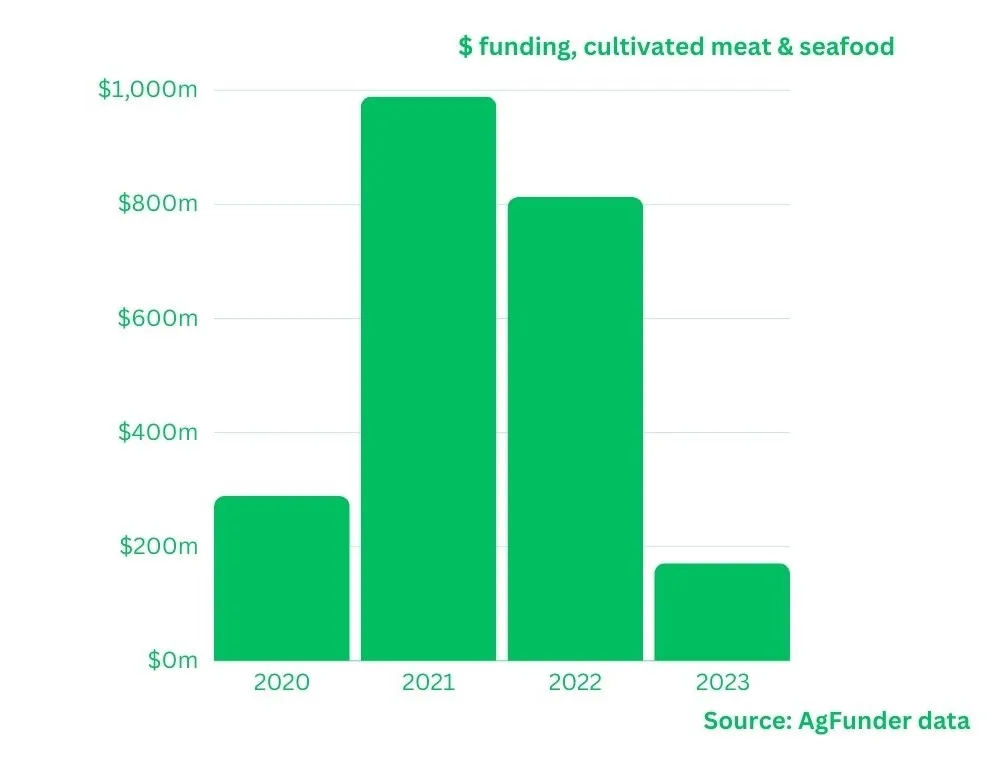

Global funding for cultivated meat & seafood startups from 2020 to 2023 (AgFunder data). Investment soared to nearly $1 billion at its 2021 peak before plummeting to under $200 million in 2023 (Cultivated meat funding nosedives in 2023).

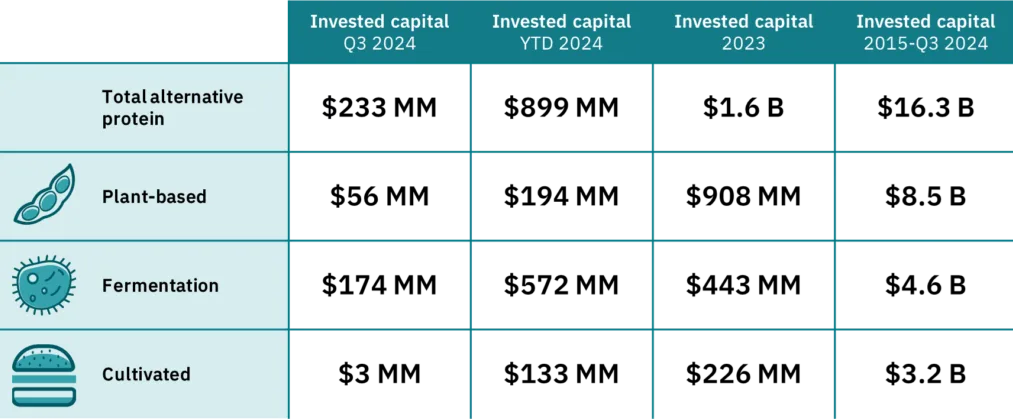

After the dramatic decline in 2023, investment levels in 2024 remained subdued but showed signs of stabilising. Preliminary data indicate 2023 saw only about $177 to $226 million raised by cultivated meat companies worldwide (Cultivated meat funding nosedives in 2023) (State of the Industry Report: Cultivated meat and seafood | GFI), a drop of roughly 75 to 80% from 2022’s total ($800+ million). In 2024, funding continued to flow, though big mega-rounds were absent. The largest single cultivated meat raise in my research was in 2024 for Mosa Meat at €40 million ($42M) in the Netherlands (The Top 10 Alt-Protein & Future Food Funding Rounds of 2024), which stood as the biggest cell-meat deal since 2022. Multiple startups secured smaller Series A/B rounds in the $10 to $40M range, which kept the yearly total in only the low hundreds of millions. Exact 2024 figures are in the process of being tallied, but overall alternative protein investment (which includes cultivated meat) was down about 27% year-on-year (Global Agrifood Tech Funding Rebounds After Two-Year Slump), suggesting cultivated meat funding in 2024 was roughly on par with, or slightly above, 2023’s depressed level. Basically, 2024 likely halted the free-fall but remained far below the highs of 2021 and 2022.

In its opening months, 2025 is showing cautious optimism. A number of cultivated meat companies announced new funding efforts or deals in early 2025, though few huge rounds have closed as of Q1. For example, Australia’s Vow was finalising a new round as of January 2025 (while, to conserve cash amid regulatory delays, simultaneously cutting 30% of staff) (Leading Cultured Meat Startup Vow Cuts 30% of Staff Ahead of Fundraise). Crowdfunding and alternative financing have also emerged. Mosa Meat quickly raised over €1.5M from small investors in a 2025 crowdfunding campaign, hitting its target within minutes (showing public enthusiasm). Overall, investor sentiment appears to be slowly improving in 2025 compared to 2024. Many investors feel the market may have “bottomed out” in 2023 and 2024, with one report suggesting that 2024’s slight uptick “hints at better days to come” (Global Agrifood Tech Funding Rebounds After Two-Year Slump). However, the rebound is tentative, fundraising remains difficult, and 2025’s full investment total is hard to predict (2025’s biggest cultivated meat trends).

Investors and Venture Capital

Despite the recent lean times, cultivated meat continues to attract a mix of specialised investors, mainstream VCs, and strategic backers.

Deep-Tech & Climate-Focused VCs

Funds like Lowercarbon Capital (which led major rounds for startups like Mosa Meat and Uncommon) (The Top 10 Alt-Protein & Future Food Funding Rounds of 2024) (Cultivated meat funding nosedives in 2023), Breakthrough Energy Ventures (Bill Gates’s climate fund), SOSV/IndieBio (early accelerator for many cell-ag startups), and Unovis (New Crop Capital) have been prominent. These investors are drawn by the technology’s long-term climate and market potential, even if near-term returns are uncertain. The number of unique investors plunged in 2023 (111, down from 204 in 2022) through broader venture pullbacks (State of the Industry Report: Cultivated meat and seafood | GFI), but top believers in the space have largely remained engaged.

Sovereign Wealth and Nation-Backed Funds

Temasek Holdings (Singapore) and Qatar Investment Authority have made large bets on cultivated meat. Temasek has stakes in leading startups like Upside Foods and Eat Just’s GOOD Meat division (Beyond Meat : Lab-grown meat producer Memphis Meats raises $161 million in funding led by SoftBank -January 22, 2020 at 07:56 pm EST | MarketScreener), and it helped bankroll Upside’s record $400M Series C in 2022 (Cultivated meat funding nosedives in 2023). Middle Eastern funds from the UAE, Qatar, and Saudi Arabia have likewise invested in companies and infrastructure (e.g. funding commercial production hubs in the Gulf). This reflects the government’s interest in food security and tech leadership.

Cultivated Meat and Seafood Funding by Year and Company (US$ millions; grand total $2,262.3M)

| Year | Company / round | Amount (US$M) |

|---|---|---|

| 2020 | Year total | 273.1 |

| 2020 | Memphis Meats (Round 1) | 161 |

| 2020 | Mosa Meat (Round 1) | 55 |

| 2020 | Mosa Meat (Round 2) | 20 |

| 2020 | Shiok Meats (Round 1) | 12.6 |

| 2020 | IntegriCulture | 7.4 |

| 2020 | SciFi Foods (Round 1) | 6.1 |

| 2020 | Avant Meats (Round 1) | 3.1 |

| 2020 | Shiok Meats (Round 2) | 3 |

| 2020 | New Age Meats (Round 1) | 2.7 |

| 2020 | Mosa Meat (Round 3) | 2.2 |

| 2021 | Year total | 911.8 |

| 2021 | Believer Meats (Round 1) | 347 |

| 2021 | GOOD Meat (Round 1) | 170 |

| 2021 | Aleph Farms | 105 |

| 2021 | GOOD Meat (Round 2) | 97 |

| 2021 | BlueNalu (Round 1) | 60 |

| 2021 | Meatable (Round 1) | 47 |

| 2021 | Believer Meats (Round 2) | 26.8 |

| 2021 | New Age Meats (Round 2) | 25 |

| 2021 | Mission Barns | 24 |

| 2021 | Shiok Meats (Round 3) | 10 |

| 2022 | Year total | 719 |

| 2022 | UPSIDE Foods (the former Memphis Meats) | 400 |

| 2022 | Wildtype | 100 |

| 2022 | Vow | 49.2 |

| 2022 | Gourmey | 47.6 |

| 2022 | Finless Foods | 34 |

| 2022 | Ivy Farm Technologies | 22.6 |

| 2022 | Hoxton Farms | 22.2 |

| 2022 | SciFi Foods (Round 2) | 22 |

| 2022 | Avant Meats (Round 2) | 10.8 |

| 2022 | CellX (Round 1) | 10.6 |

| 2023 | Year total | 165.8 |

| 2023 | Meatable (Round 2) | 35 |

| 2023 | BlueNalu (Round 2) | 33.5 |

| 2023 | Uncommon (the former Higher Steaks) | 30 |

| 2023 | Bluu Seafood | 17.5 |

| 2023 | CellMEAT | 13.2 |

| 2023 | Future Fields (growth factors) | 11.1 |

| 2023 | WandaFish | 7 |

| 2023 | Clever Carnivore | 7 |

| 2023 | CellX (Round 2) | 6.5 |

| 2023 | Meatafora | 5 |

| 2024 | Year total | 160.9 |

| 2024 | Prolific Machines (Round B1 2024) | 55 |

| 2024 | Mosa Meat (Round 2024) | 42.4 |

| 2024 | BlueNalu (Round 2024) | 33.5 |

| 2024 | Uncommon (Round A 2024) | 30 |

| 2025 | Year total | 31.7 |

| 2025 | Aleph Farms (2025) | 29 |

| 2025 | Mosa Meat (Crowdfunding 2025) | 1.6 |

| 2025 | Re:meat (2025) | 1.1 |

| 2025 | Vow (Series B, 2025) | 0 |

Corporate Strategic Investors

Major food industry players have taken equity positions. For example, Tyson Foods (the U.S. meat giant) acquired ~5% of Beyond Meat pre-IPO and invested early in Upside Foods (Memphis Meats) and Israel’s Future Meat (Believer Meats) (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). Cargill (agribusiness) also backed Upside and others. To acquire Spanish startup BioTech Foods and build a cultivated meat R&D centre, JBS (the world’s largest meat processor, Brazil) committed $100M in 2021 (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). Other corporates include Nestlé (partnering with Israel’s Future Meat) (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine), Merck KGaA (via its venture arm M Ventures in Mosa Meat), and various Asian food conglomerates. These strategic investors provide capital and scaling expertise, though some have since focused more on partnerships and R&D than large new equity infusions.

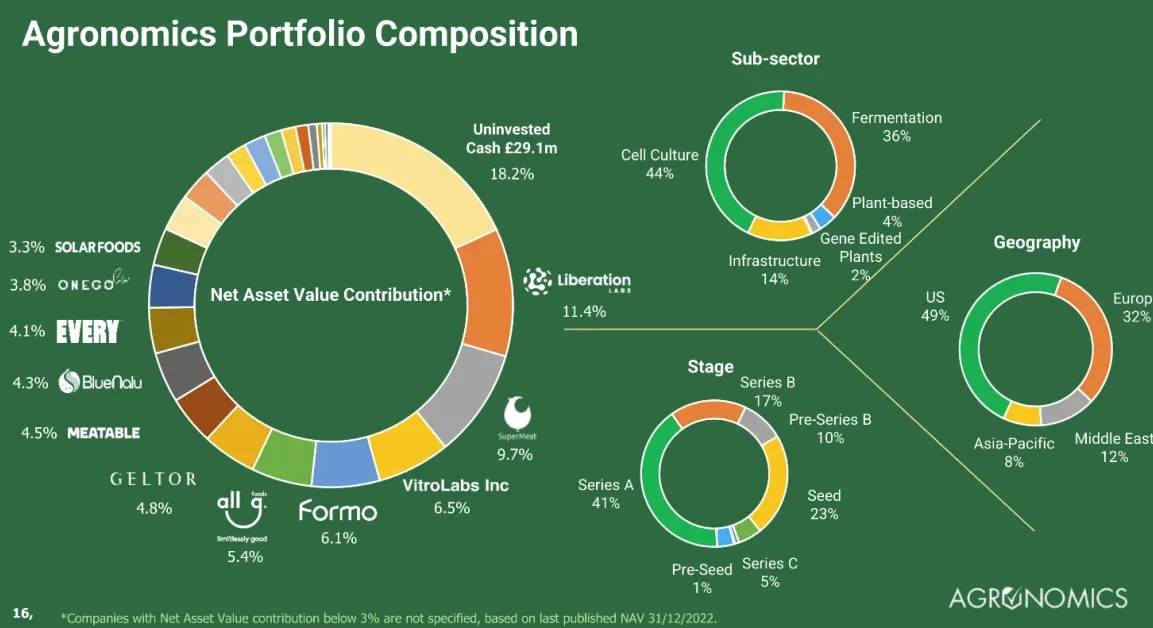

source: Agronomics

VC/PE Firms

Traditional venture capital has been selective but present. Firms like SoftBank, Norwest Venture Partners, and Richmond Global led Upside/Memphis Meats’ $161M Series B back in 2020 (Beyond Meat : Lab-grown meat producer Memphis Meats raises $161 million in funding led by SoftBank -January 22, 2020 at 07:56 pm EST | MarketScreener). Balderton Capital co-led a $30M round for UK’s Uncommon (the former Higher Steaks) in 2023 (Cultivated meat funding nosedives in 2023). Andreessen Horowitz and Khosla Ventures have invested in cell-ag adjacent tech (e.g. fermentation companies and support technologies). Additionally, Agronomics Ltd., a UK-listed investment fund for cellular agriculture, has emerged as a key investor in many startups; to provide early capital, it often joins rounds. Agronomics reports an IRR of over 20% to date on its portfolio, though these are largely unrealised gains (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)).

Source: Yahoo!finance

Angels and Others

High-profile angel investors have also backed the space. Bill Gates and Richard Branson were early backers of Upside/Memphis Meats (Beyond Meat : Lab-grown meat producer Memphis Meats raises $161 million in funding led by SoftBank -January 22, 2020 at 07:56 pm EST | MarketScreener), and Leonardo DiCaprio has invested in multiple cultivated seafood startups. Smaller mission-driven funds like Stray Dog Capital and Big Idea Ventures have seeded dozens of alt-protein companies. Their continued involvement provides a pipeline of emerging startups despite the funding downturn.

So What?

In 2024 and 2025, many of these investors became more cautious, often reserving follow-on capital for existing bets rather than making numerous new bets. However, confidence endures. Temasek publicly “remains bullish” on the space, seeing a potential $1 trillion market in alternative proteins (Temasek defends faux-meat valuations in US$1 trillion market space). Strategic partners like Tyson and JBS are hedging their bets, ensuring they have a foothold in lab-grown meat in case it disrupts conventional meat in the long run (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). Going forward, one trend is increased co-investment by government or philanthropic funds alongside VCs (for example, the Bezos Earth Fund’s $30M grant to a new cultivated protein research centre in Singapore (Singapore alternative meat startups target resurgence after sector …)). Such funding blends could help bridge the gap for capital-intensive cultivated meat projects, which pure commercial VC might shy away from in 2025.

Bloomberg Forecast for Plant-Based Meat & Dairy Retail Sales

| Year | Retail sales (US$B) |

|---|---|

| 2020 | 29.4 |

| 2030 (forecast) | 162 |

Potential Revenue from a Global US$1T Meat Industry

| Market share | Revenue (US$B) |

|---|---|

| 5% | 50 |

| 10% | 100 |

Regional Investment Trends

North America (especially the U.S.) has historically led in total investment dollars, thanks to big-ticket funding rounds for companies like Upside Foods, Eat Just/GOOD Meat, and Believer Meats. The U.S. hosted the first pilot restaurant launches of cultivated meat in 2023 (post-FDA/USDA approval), which added momentum and media exposure. However, venture funding in the U.S. cooled particularly in 2022 to 2024 due to macroeconomic factors (State of the Industry Report: Cultivated meat and seafood | GFI). Investors in Silicon Valley and beyond grew more selective, and some U.S. startups (e.g. Finless Foods, New Age Eats) had to downsize or shut down when capital ran scarce (Cultivated meat funding nosedives in 2023). Public support in the U.S. is growing, though, aiming to boost the field’s infrastructure and safety research, the federal government announced research grants and launched a USDA-funded cultivated meat consortium in late 2024 (a positive signal to investors).

Europe has been a mixed picture. The Netherlands and Israel stand out as innovation hotspots, while overall European venture funding for foodtech has been in decline (Global Agrifood Tech Funding Rebounds After Two-Year Slump). The Netherlands is home to Mosa Meat and Meatable, two of the leading cultivated meat startups in terms of funding and technical progress. Mosa Meat’s 2024 raise drew support from European investors and even government-backed funds (The Top 10 Alt-Protein & Future Food Funding Rounds of 2024). The EU’s regulatory stance remains cautious (no approvals for human consumption as of 2025), which somewhat dampens investor enthusiasm in Europe (2025’s biggest cultivated meat trends). Europe has substantial public funding initiatives: the UK government allocated £12 million (~$15M) in 2023 to a cultivated meat research hub at Bath University (State of the Industry Report: Cultivated meat and seafood | GFI), and the EU and national governments have issued R&D grants. Israel often gets grouped with Europe/Middle East in analysis; it has been a central hub, with over a dozen startups and heavy state-supported tech R&D. Israel advanced regulatory approval for cultivated beef in 2024 (one of the first countries to do so) (State of the Industry Report: Cultivated meat and seafood | GFI), and Israeli startups like Aleph Farms and Future Meat (Believer) raised some of the largest rounds in the industry’s early years. However, the industry faced challenges. To stay afloat, Aleph Farms had to seek emergency funds in 2025 (Aleph Farms raised $140 million, but now it’s struggling to survive | Ctech), indicating that even leading regions are exposed to the funding crunch.

Asia-Pacific investment is rising, led by Singapore, China, and Japan. Singapore was the first country to approve cultivated meat in 2020, and has positioned itself as an Asia cell-ag hub. To support startups, state investor Temasek and others launched the Singapore Food Tech Innovation Center and production facilities. This region has also seen notable deals: e.g. to expand into red meat tech, Singapore’s Shiok Meats acquired another startup (Gaia Foods) (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine), and cultivated seafood companies like BlueNalu and Avant Meats have attracted capital to scale up in East Asia. China’s government is heavily funding cultivated meat research (including it in its five-year agricultural plan), and Chinese startups like CellX have opened pilot plants, though most of the funding remains domestic and sometimes opaque. Japan has a growing cellular agriculture scene with startups like IntegriCulture, and large corporates (Nissan, Itoham, Mitsubishi) investing in or partnering on cell-meat projects. Across Asia-Pacific, regulatory support and public-private partnerships are shaping investment: governments in Japan, South Korea, China, and Singapore have all put cultivated meat on their national agendas (State of the Industry Report: Cultivated meat and seafood | GFI), which encourages regional investors to get involved despite the early stage. Asia-based VCs and food companies contributed roughly 30% of global cultivated meat startups as of 2025 (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine), reflecting how important this region has become in the funding landscape.

Other regions are nascent but meaningful. In the Middle East, countries like the United Arab Emirates and Qatar have poured money into cultivated meat via sovereign funds; to transfer the tech locally over time, they have often invested in Western startups. For example, to build a cultivated meat factory, Abu Dhabi’s state holding company partnered with Eat Just. Israel (covered above) is a regional leader in the Middle East. Latin America and Africa are trailing, Latin America has, to date, only a couple of startups (e.g. one in Argentina) (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine), and Brazil’s JBS is the primary investor presence from that region. Africa has seen its first cultivated meat startups (e.g. Mzansi Meat in South Africa), but investment there is minimal to date (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine). Largely, North America and Europe continue to account for most venture capital dollars in cultivated meat. Still, Asia and the Middle East share both startups and funding. This international spread is partly driven by local policy. E.g. India 2024 invested in alt-protein R&D and saw its first cultivated meat prototypes, potentially creating a new market in South Asia as well (Global Agrifood Tech Funding Rebounds After Two-Year Slump).

Agrifood Tech Funding 2024: Funding vs. Year-over-Year Change

| Region | 2024 funding (US$B) | YoY change |

|---|---|---|

| Global | 16.0 | −4% |

| US | 6.6 | +14% |

| India | 2.5 | +215% |

| China | 0.848 | −51% |

| UK | 0.616 | −45% |

| Netherlands | 0.614 | +118% |

| Finland | 0.389 | +403% |

| Japan | 0.290 | +76% |

2025 Funding Rounds and Acquisitions

2024 Highlights

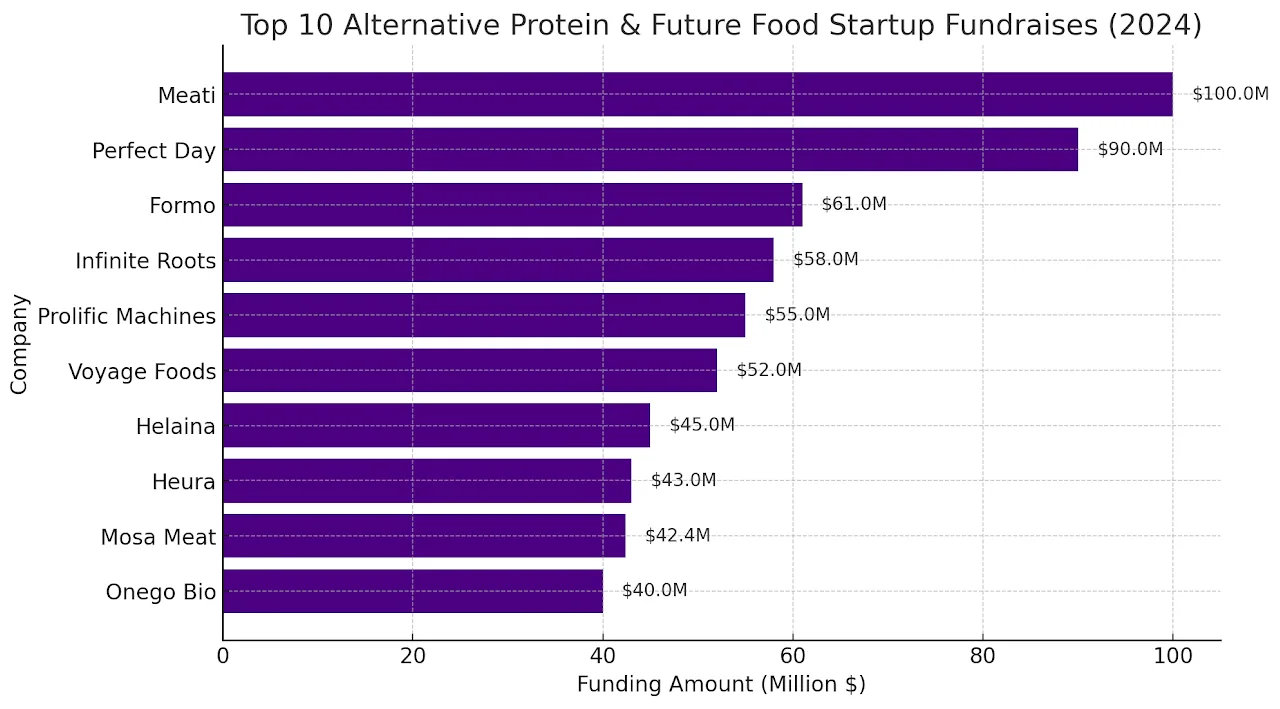

In the absence of blockbuster mega-deals, 2024 saw a series of mid-sized funding rounds, which kept many companies moving forward. Aside from Mosa Meat’s €40M noted above, other notable 2024 raises included: Meati Foods (U.S. mycelium-based meat, $100M), Perfect Day (U.S. precision fermentation dairy, $90M), and Formo (Germany, fermented dairy, $61M) (The Top 10 Alt-Protein & Future Food Funding Rounds of 2024). These are alternative protein deals adjacent to cultivated meat, underscoring that investors often look at the broader “future food” space. For cultivated meat “specifically”, to improve production technology, companies like Prolific Machines (U.S., cell-meat-enabling biotech, $55M in 2024) drew funding from notable backers like Bill Gates’s Breakthrough Energy Ventures (The Top 10 Alt-Protein & Future Food Funding Rounds of 2024). Another significant 2024 event was Lowercarbon Capital and others investing in startups like Uncommon (UK) and BlueNalu (USA); to progress cultivated pork and fish respectively, both raised around $30 to $33M (Cultivated meat funding nosedives in 2023). Such rounds, while smaller than the 9-figure raises of prior years, were lifelines, which kept R&D on track during the downturn.

2025 Funding Rounds

By early 2025, a few fresh deals signalled that capital was indeed trickling back. In January 2025, to fuel its expansion, Vow (Australia) was finalising a new round (amount undisclosed), notably after it achieved multi-market regulatory approvals for its cultured quail product (Leading Cultured Meat Startup Vow Cuts 30% of Staff Ahead of Fundraise). Vow’s fundraising suggests existing investors remain willing to fund top performers in the space. Upside Foods and GOOD Meat (the two sellers of cultivated chicken in the U.S.) have hinted at pursuing additional financing in 2025 as they prepare for larger-scale commercialisation, though no new rounds had been publicised by Q1. In parallel, startups are exploring creative financing: Mosa Meat’s rapid crowdfunding success in 2025 (raising over $1.5M from the public in minutes) demonstrated strong retail investor interest in cultivated meat’s mission (Mosa Meat Smashes Crowdfunding Goal, Raising €1.5M in Just 24 …). On the corporate side, there’s speculation that primary food companies will step in, acquiring or heavily investing in struggling startups at discounted valuations, potentially making 2025 a year of consolidation. For instance, if a firm like Aleph Farms cannot secure enough runway, it could become an acquisition target for a larger food or pharma company with an eye on absorbing its technology.

Acquisitions and M&A

To date, the cultivated meat sector has seen limited M&A, but a few deals stand out. JBS’s 2021 acquisition of BioTech Foods (Spain) (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)) was one of the first large buyouts and was intended to give JBS a foothold in cell-based protein. In 2022, to integrate cultivated fat technology for hybrid products, Steakholder Foods (Israel, the former MeaTech) acquired Belgian startup Peace of Meat. To broaden into red meat tech, Shiok Meats (Singapore) acquired a fellow startup (Gaia Foods) (Cultivated Meat: Latest News 2025 - vegconomist: the vegan business magazine). These acquisitions were mostly pre-2024, but they set the stage for what could come. In 2025, as valuations have come down, we may see new acquisitions: large meat companies or food multinationals could pick up distressed cultivated meat startups at bargain prices, or, to pool resources, stronger startups might merge. Industry insiders have called 2025 a potential inflexion point: weaker players may not survive the costly “valley of death” of scaling without merging or being acquired. One notable development is the entry of food-tech SPACs and holding companies, such as publicly-listed Agronomics (UK) and CULT Food Science (Canada), which act as roll-up vehicles with investments in many cell-ag firms. They take equity stakes in place of traditional acquisitions, which is another route by which the sector is consolidating. In 2025 to date, no headline-grabbing acquisition has been announced in cultivated meat, but rumours persist that struggling pioneers (like Aleph Farms or smaller U.S. startups) are in talks with potential buyers.

Source: GFI

Public Market Sentiment and Stock Performance

Investor sentiment in the public markets remains lukewarm and awkward for cultivated meat, given the sector’s early stage and recent setbacks. No prominent cultivated meat startup has gone public via IPO to date, reflecting both the immaturity of the revenue stage and cautious market sentiment after the broader alt-protein bubble deflated. The only pure-play cultivated meat company on the Nasdaq, Steakholder Foods (STKH, Israel), has seen its stock struggle to maintain compliance, trading under $1 for an extended period (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). As of late 2024, Steakholder’s market cap had dwindled to single-digit millions, and it faced the risk of being delisted to OTC markets (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). This poor stock performance underscores public investor scepticism; even though Steakholder holds promising 3D-bioprinting meat technology and patents, the timeline to profitability is distant, and the market is risk-averse at present. Similarly, CULT Food Science (a Canadian-listed investment vehicle for cell-ag) trades at penny-stock levels. These examples illustrate that pure cultivated meat equities have, to date, failed to win over mainstream investors.

Instead, many public market investors in search of exposure to alternative proteins have turned to proxy stocks and diversified plays. Large corporations with cultivated meat investments, such as Tyson Foods (NYSE:TSN) and JBS (BVMF:JBSS3), are considered safer bets (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). Tyson and JBS are multi-billion-dollar meat companies, whose core business is conventional protein, but they each have internal venture arms and partnerships in cell-based meat. Their stocks move based on traditional meat revenues, but if lab-grown meat succeeds long-term, these giants could benefit via their early stakes. This way, investors gain upside exposure without betting on a single unproven startup. Another publicly traded entity, Agronomics (LSE:ANIC), provides a venture-style portfolio of dozens of cell-ag startups. Agronomics has reported a ~23% IRR to date (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)), but that figure largely reflects valuation marks during the 2021 boom; its stock price has been volatile and down from highs, mirroring the sector’s cycle.

Overall, the public market sector’s attitude towards cultivated meat in 2024 and 2025 is cautious. The hype behind Beyond Meat’s soaring stock after its 2019 IPO (making “fake meat” a market darling briefly) has subsided (Leaner Times Persist For Alt Protein Funding). Beyond Meat’s subsequent crash and the underperformance of other plant-based food stocks cast a shadow on all alternative proteins, making investors wary of overhyped predictions. The stock market will likely remain sceptical until cultivated meat companies demonstrate commercial traction, revenue, production scaling, cost reduction, and consumer acceptance. That said, sentiment could shift quickly with a major catalyst. For instance, if a cultivated meat company announces a mass retail launch or margins improve faster than expected, public markets might warm up. At present, though, cultivated meat is viewed as a long-horizon, speculative segment. Market analysts in early 2025 characterise it as a “risky business for investors” with a certain timeline (2025’s biggest cultivated meat trends), which explains the hesitance in public equity markets.

Challenges Influencing Investment Trends

Several key challenges have been influencing cultivated meat investment trends in 2024 and 2025.

High Costs and Scale-Up Hurdles

The cost of producing cultivated meat remains vastly higher than conventional meat. Achieving cost parity requires major scientific breakthroughs and economies of scale in bioprocessing. As one analysis put it, the industry “uses a lot of high-tech solutions and highly-trained scientists, but it has to compete with just feeding and killing a cow”, so scaling up efficiently is paramount (Top 5 Lab-Grown Meat Stocks to Invest In (March 2025)). Difficulties in upscaling production may deter investors in 2025 (2025’s biggest cultivated meat trends). Many startups are stuck in the pilot phase, needing expensive bioreactors and cell culture media. This challenge has created a “valley of death” between proof-of-concept and commercialisation, in which additional funding is hard to secure (A weak $11.3bn start to 2024). The result: to survive until costs come down, companies either raise bridge rounds at down valuations or slow their burn (e.g. Vow’s staff cuts). Until there is proof that cultivated meat can be mass-produced affordably, some investors will remain on the sidelines.

Regulatory Uncertainty and Pace

Gaining regulatory approval is mandatory before selling cultivated meat, and the process is lengthy and complex. By the end of 2024, only a handful of countries (Singapore, U.S., Israel) had approved limited products, and no approvals had come from the EU or UK (2025’s biggest cultivated meat trends). Long waits for regulators to green-light products (especially in Europe) can make investors reluctant to fund companies with revenue potentially years away (2025’s biggest cultivated meat trends). In the U.S., while the first approvals are in hand, ongoing political and legal uncertainty exists. For example, in 2024, some U.S. states like Florida and Alabama even passed preemptive bans on cell-cultured meat sales (February 2025 - The Council of State Governments) pending federal oversight, adding another layer of risk. The good news is that 2023 and 2024 saw momentum in regulatory milestones (USDA approvals, Israel’s OK for beef, etc.), but for most markets, the timeline remains a bottleneck. This challenge influences investment by favouring companies in jurisdictions with clearer paths (hence the interest in Singapore/U.S. startups) and increasing the importance of regulatory strategy in due diligence.

Investor Fatigue & Dilution

After the exuberance of 2020 and 2021, many of the investors behind the alternative protein boom have pulled back, citing slower-than-expected progress. The cultivated meat field, in particular, has been accused of over-promising timelines. The steep funding drop in 2023 (State of the Industry Report: Cultivated meat and seafood | GFI) was partly due to “general risk aversion” amid economic uncertainty (Cultivated meat funding nosedives in 2023) but also a recalibration of expectations. Companies with prior raises at high valuations sometimes have to raise down-rounds (e.g. Aleph Farms’ valuation cut ~75% in 2025) (Aleph Farms raised $140 million but now it’s struggling to survive | Ctech), causing prior investors to take losses or get diluted. This dynamic creates hesitation to re-invest. Many venture funds also faced their own capital crunch in 2023 and 2024, meaning less dry powder for niche bets like cell-ag. As a result, even promising startups struggled to find new lead investors, and the pace of new company formation slowed. As funding for brand-new entrants is scarce, the number of new cultivated meat startup announcements has tapered off compared to the flurry a few years ago.

Technical and Taste Questions

While tremendous technical progress has been made, challenges remain in replicating the taste/texture of whole-cut meats, ensuring long-term cell line stability, and sourcing cost-effective growth media. Some investors are concerned about unresolved technological hurdles; for example, can growth factor costs be lowered 1000-fold? Can scaffolding yield a steak truly akin to a ribeye? These are open questions. Additionally, consumer acceptance remains uncertain; surveys show curiosity but also some scepticism about eating meat from a bioreactor. This creates a market risk on top of the technical risk. At this stage, limited consumer trials (tasting events in restaurants) have been positive, but broad acceptance will only be tested on a larger scale.

Market Competition and Alternatives

The investment case for cultivated meat also depends on what happens with alternative solutions. Plant-based meat, fermentation-derived proteins, and even novel proteins (insects, etc.) all vie for the “sustainable protein” market. If, for example, plant-based meat significantly improves or regains growth, it could reduce the addressable market for cultivated meat or at least elongate the timeline. Investors weigh these scenarios. Plant-based meat companies like Beyond Meat have struggled with sales, but fermentation (e.g. precision fermented dairy, mycoprotein) is making quiet inroads. Cultivated meat startups have responded by exploring hybrid products; to reach price points and improve texture, these blend plant and cell components (e.g. cultivated fat combined with plant protein burgers). This competition and potential collaboration blur the lines, but it also means that cultivated meat is one of several approaches to disrupting conventional meat, which can temper some investors’ sense of urgency.

Opportunities and Positive Drivers

Despite the challenges, several opportunities are driving optimism and investment interest in 2025.

Regulatory Breakthroughs & Market Debuts

The fact that cultivated meat is on sale (albeit in limited venues) to real consumers is hugely significant. The U.S. approvals in 2023 and Israel’s in 2024 proved that regulators are willing to give the green light (State of the Industry Report: Cultivated meat and seafood | GFI). This has inspired confidence that cultivated meat is inevitable, even if the timing is uncertain (2025’s biggest cultivated meat trends). With more countries likely to approve sales in 2025 to 2026 (e.g. UK, EU possibly by 2025/26 for existing submissions (2025’s biggest cultivated meat trends)), investors see the potential for new markets opening. Each regulatory win de-risks the sector: for instance, when the FDA cleared Upside’s chicken as safe in late 2022, it removed a huge question mark. The focus shifts to market execution, which is an opportunity for companies to generate early revenue and for investors to see commercial validation. The entry of cultivated meat into high-end restaurants (in Singapore, the U.S., and, as of 2025, Hong Kong) has created buzz and demand far in excess of the tiny supply. This pent-up demand is an encouraging sign to investors that when production scales, there will be willing customers.

Continuing Government and Academic Support

As mentioned, several governments are putting money into cultivated meat research and infrastructure. The UK’s grant funding, the EU’s research programmes, China’s public research funding, and Japan’s government-led initiatives all represent non-dilutive funding pumping into the field (State of the Industry Report: Cultivated meat and seafood | GFI). Establishing innovation hubs (e.g. the Bezos Earth Fund’s Sustainable Protein Center in Singapore (Singapore alternative meat startups target resurgence after sector …), and a sister centre at UC Davis in the U.S., will produce IP and skilled talent for startups to leverage. For investors, public co-investment reduces some risk and signals that policymakers are serious about enabling this industry (important for long-term market creation). Additionally, forming industry alliances and open-access research (such as GFI-funded studies on improvements to growth media and cell line development (State of the Industry Report: Cultivated meat and seafood | GFI)) helps the entire sector advance. These efforts could shorten the time to technical milestones, improving the investment outlook.

Technological Strides

Even in the lean funding period, science has marched on. Researchers and startups have made progress in lowering costs; for example, innovative continuous production methods for cultivating cells (rather than batch bioreactors) were demonstrated, promising orders-of-magnitude efficiency gains (2025’s biggest cultivated meat trends). Improvements in cell culture media (finding cheap, plant-derived ingredients to replace expensive pharma-grade components) have been documented (State of the Industry Report: Cultivated meat and seafood | GFI). And new product possibilities (like structured steaks, cultivated fish fillets, and exotic meats) are expanding the horizon beyond only ground meat. Each technical breakthrough (patents on new scaffolds, better cell densities, etc.) is an opportunity for value creation, either as IP licensing or as a competitive advantage for a startup. Investors are looking for companies capable of crossing key cost or scale thresholds, as that could unlock a massive first-mover advantage in the market. The first company to truly achieve cost-competitive cultivated chicken or beef would likely attract a rush of capital (even an IPO) given the multi-billion dollar market in waiting.

Climate and ESG Momentum

The fundamental driver for cultivated meat remains its promise of a far lower environmental footprint and freedom from industrial farming cruelties. With climate change and sustainability as top global concerns, the ESG (Environmental, Social, Governance) investment theme continues to favour alternative protein development. Many institutional investors have mandates to invest in climate solutions, and food/ag is a significant part of emissions. Cultivated meat could reduce land, water, and emissions by a large margin if powered by clean energy. While renewable energy and electric vehicles have been grabbing most climate investment, the relative underinvestment in sustainable food (only ~$3B all-time in cultivated meat vs. tens of billions in climate-tech energy) (State of the Industry Report: Cultivated meat and seafood | GFI) is starting to get noticed as an opportunity. Some venture firms and corporate investors see 2025 to 2030 as the period for alt-protein to catch up as a critical climate tech sector. This narrative of “feeding 10 billion people sustainably” is helping keep patient capital interested. Cultivated meat companies can sometimes access impact investment funds or blended finance beyond the reach of typical startups, giving them an extended runway.

Consumer Interest and Media Attention

Though consumers have barely gotten to try cultivated meat, interest levels are high. Media coverage in 2024 (from cultivated meatballs on prime-time TV (Leading Cultured Meat Startup Vow Cuts 30% of Staff Ahead of Fundraise) to extensive press on the first restaurant tastings) kept the topic in the public eye. Surveys show a significant fraction of consumers globally are willing to try or buy cultivated meat at least once. Younger demographics, in particular, align the product with tech-forward climate action. This public interest is an opportunity for future growth; when products hit the market at scale, early adopters could drive strong sales. For investors, the public sentiment represents potential demand. We saw how the plant-based meat craze created a wave of trial and adoption around 2019; something similar could happen with cultured meat when available. Public market sentiment could also turn positive if, for example, a cultivated meat company lists on an exchange and markets the stock as the next big sustainable tech story. In essence, the storyline of “reinventing meat” continues to hold strong appeal, and if costs decline and availability increases, a second wave of hype (hopefully matched by substance) could greatly benefit the sector.

Resurgence of 2025?

Has the cultivated meat sector seen a resurgence in investment in 2025? The data and observations to date suggest a gradual recovery, short of a dramatic resurgence. After hitting a low point in 2023, the sector’s funding climate stabilised in 2024, and 2025 shows early signs of renewed activity. Global agrifood tech funding overall was flat in 2024 after two years of decline (Global Agrifood Tech Funding Rebounds After Two-Year Slump), indicating the worst may be over. In cultivated meat, the free-fall in investment has stopped, and optimistic investors are tiptoeing back in, albeit carefully. There is a sense of “cautious optimism” among VCs and industry observers that 2025 could begin a rebound, primarily if a few more milestones (technical or regulatory) are achieved. Indeed, some investors believe the sector is bottoming out and poised for better days ahead (Global Agrifood Tech Funding Rebounds After Two-Year Slump).

However, it would be premature to call it an outright resurgence. Funding volumes in early 2025 remain a far cry from the record levels of a few years ago. Many companies continue to operate on tight budgets, and new funding often comes with tough terms (down rounds, structured equity, etc.). Public market sentiment remains sceptical, and no new cultivated meat IPOs have tested investor appetite. In essence, 2025’s investment climate is one of consolidation and selective bets: money is available for the top performers, and most promising technologies, but indiscriminate funding of any “lab meat” idea (as seen in 2021) is over. The recovery is uneven. Some regions (North America, parts of Asia) and some investors (strategic corporates, mission-aligned funds) are quicker to re-invest than others.

Suppose companies can use 2025 to demonstrate tangible progress (e.g., hitting cost targets of ~$10 per pound, securing regulatory approval in Europe, or launching products in more restaurants). In that case, it will likely unlock a resurgence of investor enthusiasm in late 2025 and beyond. The foundations for that future growth are being laid: continued R&D, government support, and the first trickle of revenue from pilot sales. As one VC noted, recent approvals have shown the “inevitability” of this technology (2025’s biggest cultivated meat trends).

The cultivated meat sector in 2025 is cautiously climbing out of a downturn. Total investment is modestly up from 2023’s nadir, key investors are staying the course (with a few new entrants), and regional support is growing in Asia and elsewhere. But challenges in scale and economics temper the pace of growth. The term “resurgence” might be slightly strong for the current state; “slow recovery” may be more accurate. The trajectory is positive, and if breakthroughs continue, we could see a more vigorous resurgence in the coming quarters. Cultivated meat remains a long-term bet, which many investors continue to believe in but are approaching with clearer eyes and prudent strategies in 2025.

Sources

The analysis above is based on investment data and reports from industry trackers and media, including AgFunder (Cultivated meat funding nosedives in 2023), GFI (State of the Industry Report: Cultivated meat and seafood | GFI), Green Queen Media (Global Agrifood Tech Funding Rebounds After Two-Year Slump), Crunchbase News (Leaner Times Persist For Alt Protein Funding), and others, as well as specific examples of funding rounds and company news from 2024 to 2025. All citations for direct data and quotes are provided inline.