Macroeconomic analysis of Cell-Based Meat (CBM)

Investment Trends (Venture Capital, Public Funding, Private Equity)

Over the past decade, cultivated meat has evolved from a science experiment into a venture capital magnet. Cumulative private investment since 2013 reached about $3.1 billion by the end of 2023, with over 80% of that pouring in just in the last three years (2023 State of the Industry Report: Cultivated meat and seafood). Annual funding peaked in 2021 when startups raised a record $1.3 billion, followed by $896 million in 2022 (2022 Cultivated Meat Executive Summary). In 2022 the largest single deal was UPSIDE Foods’ $400 million Series C (the biggest round in the sector to date) (2022 Cultivated Meat Executive Summary). However, 2023 saw a sharp pullback. Only $225.9 million was raised globally in 2023, a steep drop reflecting the broader downturn in venture funding (2023 State of the Industry Report: Cultivated meat and seafood). This decline mirrors cautious investor sentiment amid high interest rates and recession fears (2023 State of the Industry Report: Cultivated meat and seafood). Venture capital has been the primary driver, attracting major food-tech investors and even traditional meat companies. Corporate and private equity stakeholders have joined in: for example, meat giants like JBS, Tyson Foods, and Cargill have invested in or formed partnerships with cell-cultured meat startups (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X).

Public funding is also growing as governments recognise the strategic importance of alternative proteins. In 2023, governments worldwide ramped up support, from China and Israel to Japan, the UK, and the US, investing in new research centres and pilot production facilities for cultivated meat (2023 State of the Industry Report: Cultivated meat and seafood) (2023 State of the Industry Report: Cultivated meat and seafood). The U.K. alone announced £15 million (~$19M) for a cultivated protein research hub and additional grants for cultivated meat R&D (2023 State of the Industry Report: Cultivated meat and seafood). Similarly, Japan and Singapore have issued grants to cell-ag startups, and the EU has funded consortium projects. While no cultivated meat company is publicly traded at scale (the industry is in large part pre-revenue), one Israeli company (Steakholder Foods) listed on Nasdaq, and more may pursue IPOs or SPAC deals as the sector matures. Overall, investment trends show high initial exuberance with recent consolidation, implying that only the strongest players with clear paths to scale will attract the big rounds going forward (Cultivated meat: ‘70-90% of players will fail in the next year’).

According to a new report from Oghma Partners, more than £2.6bn has been invested in cultivated meat companies since 2016, with five companies (UPSIDE Foods, Believer Meats, Wildtype, Aleph Farms, and Mosa Meat) accounting for 47% of all funds raised.

Image credit: Oghma Partners

Global Regulatory Landscape and Policy Changes

Regulation has quickly gone from hypothetical to actionable in the last few years. A major breakthrough came in Singapore in late 2020 when the Singapore Food Agency approved Eat Just’s GOOD Meat cultivated chicken, the world’s first regulatory approval for cultivated meat (C&EN). This allowed commercial sales in a Singapore restaurant, marking a historic turning point. The United States followed: in 2022, the FDA issued “no questions” approvals for the safety of UPSIDE Foods’ and GOOD Meat’s cultivated chicken, and by mid-2023, the USDA had fully approved these products for sale. Thus, in 2023, the U.S. became the second country to enable the retail sale of cultivated meat, with both UPSIDE Foods and GOOD Meat serving cultivated chicken in limited restaurants (C&EN). Israel became the third country: regulators there gave Aleph Farms the green light to sell its cultivated beef, making Israel the first to approve cultivated beef specifically (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). These early approvals in Singapore, the U.S., and Israel have created a precedent and are building confidence in the safety and oversight of cell-cultured meat.

Elsewhere, regulatory progress is underway. Europe’s regulatory landscape is cautious but evolving. The EU will treat cultivated meat as a Novel Food, requiring a European Food Safety Authority (EFSA) review. No EU approvals have occurred as of 2024, but multiple companies (Mosa Meat, for example) are preparing dossiers, and the first EU approvals are anticipated in the next 2 to 3 years if safety data satisfy regulators. The UK, post-Brexit, is independently funding cultivated meat research and has signalled openness to novel foods; in 2023, the UK government invested millions in a cultivated meat research centre, indicating a supportive stance (2023 State of the Industry Report: Cultivated meat and seafood). China has declared cultivated meat a technology of interest. It included cultivated meat and other alt-proteins in its national Five-Year Plan, signalling future regulatory and funding support. China is building its regulatory framework, and while no sales are legal there, Chinese startups (like CellX) are actively piloting products and the government is expected to approve cultivated meat when domestic companies are ready. Japan is similarly moving toward a framework by transferring novel food regulation authority and funding local companies, aiming to commercialise cultivated meat in coming years (As Japan commits to cultivated meat, will Europe be left behind?).

Not all policy moves have been supportive. Geopolitical and cultural pushback has emerged in some regions. In 2023, Italy’s government passed a law banning the production and sale of cultivated meat entirely, framing it as protecting food heritage (Italy ban on cultivated meat cuts itself off from innovation and blocks sustainable development: GFI Europe). This law would fine any cultivated meat activity and even restrict naming (it also bans using meat terms for plant-based foods) (Italy ban on cultivated meat cuts itself off from innovation and blocks sustainable development: GFI Europe). Critics argue Italy’s ban “isolates Italy from the investment and job creation” that this high-tech sector offers (Italy ban on cultivated meat cuts itself off from innovation and blocks sustainable development: GFI Europe). In the U.S., while federal regulators approved cultivated meat, a couple of state legislatures (e.g. Florida and Alabama) moved to ban sales of lab-grown meat in their states (Leading Lab-Grown Meat Company Cuts Dozens of Jobs | WIRED), largely due to agricultural lobbying and political sentiment. These counter-currents show that regulatory acceptance is not universal in local politics, and public perception can impede rollout.

Overall, however, the global trend is toward accommodation: more countries are establishing approval pathways, and international bodies are engaging (the UN’s 2022 UNEP report highlighted cultivated meat’s potential benefits (2023 State of the Industry Report: Cultivated meat and seafood), and COP28 in 2023 featured alternative proteins on the climate agenda for the first time (2023 State of the Industry Report: Cultivated meat and seafood)). In the next five years, we expect wider regulatory uptake and likely approvals in parts of Asia and Europe alongside clearer labelling and safety standards. These policy shifts will significantly shape where companies focus their launches and how quickly they can scale economically.

Supply Chain Dynamics (Materials and Costs)

Upstream materials and inputs for cultivated meat are a critical macro factor, as they determine feasibility and cost. The supply chain for cultivated meat overlaps with biopharmaceutical supplies: the industry must secure cell culture media, growth factors, scaffolding materials, and bioreactors at food-industry volumes and prices. Initially, cultivated meat relied on expensive pharma-grade inputs (notoriously, fetal bovine serum was used in early research), which made the cost of growth media astronomical. For cultivated meat to be viable, these costs have to plummet. Indeed, experts note that growth media, which can cost hundreds of dollars per litre in biotech settings, needs to fall to on the order of $1 per litre or less (C&EN). Achieving a 100x+ cost reduction in media is a huge challenge, but progress is being made. Companies are developing animal-free, food-grade media and producing growth factors via fermentation or plant expression rather than costly pharma methods. In one breakthrough, researchers at Tufts engineered bovine cells to produce their own growth factor, reducing the need for adding those expensive ingredients externally (Cultivated Meat Production Costs Could Fall Significantly with New Cells Created at Tufts | Tufts Now). This kind of innovation could dramatically cut variable costs. Surveys of suppliers suggest that within the next five years, bulk cell-culture medium costs could drop below $5 per litre and continue downward ([PDF] Cultivated meat media and growth factor trends 2020). As demand for media scales, manufacturers will transition from bespoke batches to large-scale production, driving economies of scale.

Beyond media, hardware and equipment supply chains are crucial. Cultivated meat production requires specialised bioreactors (stainless steel tanks, similar to those used in brewing or vaccine production), as well as filtration and harvesting systems. These must be food-safe and, in some cases, custom-designed for cell culture. The pandemic and subsequent supply chain snarls have shown the risk: long lead times for bioreactors or sensors could slow expansion of production capacity. Materials like pharmaceutical-grade amino acids, vitamins, and sugars (the “feed” for the cells) are subject to global commodity price fluctuations. For instance, spikes in sugar or micronutrient prices would raise operating costs for cultivated meat facilities. Companies are exploring alternative sourcing, such as using agricultural by-products or lower-cost inputs, but any change must ensure cell health and product safety. The war in Ukraine and general inflationary pressures in 2022 to 2023 led to higher prices for energy and stainless steel, indirectly affecting bioreactor costs and facility construction budgets.

Supply chain resilience is therefore a macro concern: to secure their supply and manage costs, firms are beginning to partner with established suppliers (e.g., pharma ingredient companies) or develop in-house production for critical inputs. Over the next few years, we expect to see convergence toward a dedicated cultivated meat supply chain, with input providers scaling up production of growth media components and single-use bioprocessing tools tailored for food. These developments should gradually drive down costs and smooth out material availability, though short-term fluctuations (e.g. due to inflation or trade restrictions) can impact the industry’s economics.

Source: Biotechnol. Bioeng. 2022, DOI: 10.1002/bit.28324.

Labour Market Impact and Employment Trends

The cultivated meat industry is creating a new labour niche at the intersection of biotech and food. Over the last decade, we’ve seen the number of dedicated cultivated meat companies grow from only a handful of pioneers to around 170+ companies worldwide in 2023 (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). This boom has generated demand for specialised talent: cell biologists, tissue engineers, bioprocess engineers, food scientists, regulatory experts, and even sensory chefs. In the past 5 to 10 years, hundreds of high-skilled jobs have emerged in startups and research labs focused on cell-cultured meat. Many companies are spin-offs from academia, pulling PhDs and researchers into startup roles. As startups matured, they also began hiring experts from adjacent industries (pharmaceutical biomanufacturing, food processing, etc.) to help design pilot plants and navigate compliance. This has led to job growth in high-tech R&D and engineering roles. Some estimates suggest each cultivated meat plant job can create ancillary jobs in equipment, logistics, and retail as the ecosystem develops (Cultivated meat could add up to €85 billion to the EU economy and create up to 90,000 jobs by 2050: GFI Europe). One analysis projects that by 2050, a scaled-up cultivated meat sector could create up to 90,000 jobs in the EU alone (Cultivated meat could add up to €85 billion to the EU economy and create up to 90,000 jobs by 2050: GFI Europe). While that is long-term and contingent on supportive policy, it underscores the significant employment potential in this field.

In the near term (next 5 years), the labour impact is twofold. First, continued hiring in core technology positions as companies move from proof-of-concept to commercialisation we expect growing demand for bioprocess technicians to run bioreactors, QA/QC specialists to ensure product safety, and regulatory affairs professionals to liaise with government agencies. Second, there may be shifts in the traditional meat labour market: as cultivated meat scales (post-2030), it could begin displacing a small share of conventional meat production, which might affect farming and slaughterhouse jobs. However, in the next five years, cultivated meat volumes will be too low to noticeably impact traditional agriculture employment. Instead, we might see job growth in hybrid roles, for instance, meat processing companies might hire cultured meat experts to integrate this new product line alongside conventional meat.

It’s worth noting that the industry’s recent financial tightening has tempered its hiring spree. To conserve cash, some leading startups have had to trim their workforce in 2023 to 2024 after rapid expansion in 2020 to 2021. For example, UPSIDE Foods, one of the best-funded cultivated meat startups, announced layoffs of about 26 staff in 2024, citing funding hurdles and a need to refocus on critical milestones (Leading Lab-Grown Meat Company Cuts Dozens of Jobs | WIRED). This reflects a broader trend: as venture capital cooled, companies are extending their runways, sometimes by reducing headcount. Nonetheless, overall employment in the sector remains on an upward trend as new facilities come online. Governments see the promise of high-skilled job creation. Public officials often cite alternative proteins as a growth industry for future jobs. Conversely, regions that oppose cultivated meat (like Italy with its ban) risk forgoing those future jobs and investments (Italy ban on cultivated meat cuts itself off from innovation and blocks sustainable development: GFI Europe). The cultivated meat industry is an emerging source of specialised employment and, with sustained growth, could become a notable job creator, even as it navigates the typical boom-bust hiring cycles of early-stage sectors.

Geopolitical and Economic Influences on Growth

Broad geopolitical and economic factors heavily influence the cultivated meat industry’s trajectory. A key driver at the geopolitical level is food security and sovereignty. Countries that rely on heavy meat imports or face food insecurity are viewing cultivated meat as a strategic opportunity. For instance, Singapore’s proactive approval of cultivated meat aligns with its goal to produce more food domestically (it imports >90% of food). Similarly, Middle Eastern countries and China (which worry about stable protein supplies for growing populations) have invested in cellular agriculture to reduce reliance on imports and vulnerability to livestock diseases or trade disruptions. These strategic motivations mean that in some regions, cultivated meat enjoys strong government backing as a matter of national interest. China’s inclusion of cultivated meat in its national science and technology plan is a prime example of geopolitics favouring growth: it signals to Chinese universities and investors that this is a priority area (likely leading to accelerated research funding and potentially faster regulatory approval when ready).

Climate change and sustainability goals also play a geopolitical role. The EU’s Green Deal and Farm-to-Fork strategy, for example, emphasise cutting agricultural emissions a push that indirectly benefits the case for cultivated meat as a lower-methane, land-sparing alternative. International climate commitments may encourage countries to explore cultivated meat to meet emission targets. On the flip side, traditional livestock industries remain powerful in many countries, and their lobbying can shape policy against cultivated meat. We saw this in Italy’s ban, which agricultural groups and cultural arguments influenced. Likewise, in the U.S., states with large cattle industries have quickly introduced bills restricting cell-based meat labelling or selling. These protectionist or culturally motivated policies can slow adoption in certain locales, effectively creating an uneven global playing field. Companies might focus on more receptive markets, concentrating economic growth in those regions ahead of others.

Macroeconomic conditions have a more short-term but significant impact. The high-inflation environment of 2021 to 2023 increased costs for everything from stainless steel (for tanks) to energy (for running bioreactors). Cultivated meat production is energy-intensive (temperature control, stirring, etc.), so rising electricity prices squeeze margins. Additionally, the cost of capital surged as interest rates rose sharply in 2022 to 2023. This made it more expensive to raise money or finance the construction of production plants. The result was a slowdown in new facility construction and greater emphasis on efficiency at existing pilots. We saw many startups delay ambitious expansion plans for example, UPSIDE Foods paused building a large-scale Illinois plant due to economic headwinds (Leading Lab-Grown Meat Company Cuts Dozens of Jobs | WIRED). The broader VC pullback in tech funding (partly due to recession fears and poor performances of some alternative protein companies like Beyond Meat) also hit the cultivated meat sector. In 2023, investor enthusiasm cooled, and funding became far more selective, favouring only the top players (Cultivated meat: ‘70-90% of players will fail in the next year’) (Cultivated meat: ‘70-90% of players will fail in the next year’).

Geopolitical tensions can affect supply chains and collaborations too. Export controls or trade tensions (e.g., between the U.S. and China) could limit the exchange of biotech equipment or slow down joint ventures across borders. Nonetheless, international collaboration is notable in this field, for instance, a Japanese firm partnering with Israel’s Aleph Farms to bring cultivated beef to Japan (As Japan commits to cultivated meat, will Europe be left behind?), or U.S. and Singapore agencies sharing data to streamline regulatory processes. Geopolitics also affect consumer sentiment: in some countries there is nationalist pride in being at the cutting edge of food tech (Israel and Singapore often highlight their cultivated meat firsts), whereas in others there’s scepticism of a “foreign” or “lab” product (some European farm lobbies label it as an unnatural invention from Silicon Valley).

Over the next five years, economic recovery or downturn will directly influence available investment, and a strong global economy could renew capital flow to novel tech, whereas a recession would make fundraising even tougher for these companies. Likewise, any major geopolitical threat to meat supply (for example, a new animal disease outbreak or trade embargo) could become an unexpected boon by highlighting the resilience advantage of producing meat without livestock. The growth of the cultivated meat industry is intertwined with global economic cycles, political decisions, and cross-border issues that can either catalyse its expansion or throw up roadblocks.

Market Growth Projections (Demand and Pricing Outlook)

Forecasting market growth for cultivated meat is challenging given its nascent stage, but analysts generally agree the sector will see rapid growth from a tiny base. Over the last ten years, demand was essentially theoretical. Only in the last 2 to 3 years have consumers been able to buy cultivated meat (and even so, only in limited locations like Singapore or a few U.S. restaurants). Thus, current market size (2024) is negligible in the context of the $1+ trillion global meat industry. The real inflection is expected in the coming decade. A McKinsey analysis projects the cultivated meat market could reach about $25 billion by 2030 (Cultivated meat: Out of the lab, into the frying pan | McKinsey). This would be a remarkable increase from near-zero, implying a very high compound annual growth rate as production scales. Yet even $25B would be a small fraction of the total meat market (roughly 1-2% by value in 2030), underlining that conventional meat will remain dominant through the 2020s. Other projections are even more bullish in the long run: consulting firm AT Kearney famously predicted that by 2040, 35% of all meat could be cultivated (with another ~25% plant-based), leaving only 40% from traditional slaughter (Most ‘meat’ in 2040 will not come from dead animals, says report). In the mid-term (next 5 to 10 years), however, most scenarios see single-digit percentages at most. Boston Consulting Group (BCG) and others have forecast alternative proteins (inclusive of plant-based, fermentation, and cultivated) could claim 11% of the protein market by 2035, with cultivated meat being a subsequent contributor to that mix.

In terms of demand drivers, consumer awareness and acceptance will determine how fast the market can grow when supply becomes available. Early indications are that there is strong curiosity and a sizable segment of consumers willing to try cultivated meat (more on that in the micro section), which could translate into initial demand outstripping the very limited supply. In Singapore, for example, restaurants offering GOOD Meat’s cultivated chicken have had waitlists of eager patrons. As production volume increases and more markets open, we can expect a luxury/novelty phase where cultivated meat is sold in high-end restaurants and speciality grocers at a premium price, targeting foodies and sustainability-conscious consumers. During this phase, supply and regulatory access constrain demand more than price does. The industry is likely to price products to maximise revenue but also to gather consumer data on how much people are willing to pay.

Pricing trends are thus expected to start high and gradually decline. The very first prototypes (2013’s famous cultured burger) had an astronomical implied price (hundreds of thousands of dollars). By 2020, limited tastings pegged portions in the hundreds of dollars range (though these were not true market prices). In 2023, real menu prices ranged from about $15 (in Singapore’s casual setting) to $70+ for upscale U.S. restaurant dishes (C&EN). These price points are equivalent to dozens of times the price of conventional chicken on a per-pound basis, reflecting the current scarcity and cost. As scale improves, the price per unit should fall. Some companies have publicly stated target prices. For instance, Future Meat Technologies (Believer Meats) aimed to get its cultivated chicken cost down to $5-$6 per pound in the mid-2020s, which would allow a retail price not far off premium organic chicken. Indeed, by late 2021 Future Meat reported producing chicken for $7.70 per pound ($17/kg), down from ~$18 per pound just six months prior (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year). This rapid cost decline suggests that, if similar progress is made industry-wide, the price gap vs. conventional meat will narrow. Market analysts expect that within 5 years, cultivated meat could be perhaps 2 to 3 times the cost of traditional meat, and in niche markets consumers may pay that difference. Longer-term (~10+ years), the holy grail is price parity: achieving the same or lower cost than farmed meat, unlocking mass-market potential. Whether that happens by 2030 or only much further out is debated; it depends on technical cost reductions (see microeconomic factors below).

In terms of volume growth, one can envision a trajectory where by 2030, cultivated meat moves from effectively zero to perhaps tens of thousands of metric tons produced annually worldwide. For perspective, conventional meat production is about 350 million metric tons per year. Even a very optimistic scenario might see cultivated meat approaching 1% of that volume by 2030 (a few million tons), but more conservative forecasts keep it well below 0.1% by 2030. Industry targets give a clue: UPSIDE Foods’ planned first commercial plant is aiming for 13,000 tons/year capacity at full scale (C&EN), and GOOD Meat plans a similar facility (C&EN). If those come online by ~2027 to 2028 and run near capacity, and a handful of other companies build plants, global cultivated meat output could hit perhaps ~50,000+ tons/year by 2030 in an aggressive growth case. In revenue terms, that might be several billion dollars in sales (depending on price per kg).

Thus, market growth projections for the next 5 to 10 years show a small but fast-growing industry: likely a niche luxury market through the late 2020s, expanding to broader retail by the early 2030s as costs fall. Price trends should move downward over time. One report even noted that Mark Post, creator of the first lab burger, saw his effective cost go from $330,000 per burger in 2013 to about $11 per burger (roughly $80/kg) within a few years (Today was the first commercial sale of cell-cultured meat in human …). While that $80/kg remains very high, it signals the direction of change. Stakeholders forecast double-digit or higher annual growth rates for this sector well into the 2030s (AT Kearney expects alternative meats to make up 60% market in 2040: The Futures Centre), contingent on supportive economics and consumer uptake. The cultivated meat market is poised to grow from virtually nothing to potentially billions in value within a decade, albeit with significant uncertainty around the exact pace and scale of adoption.

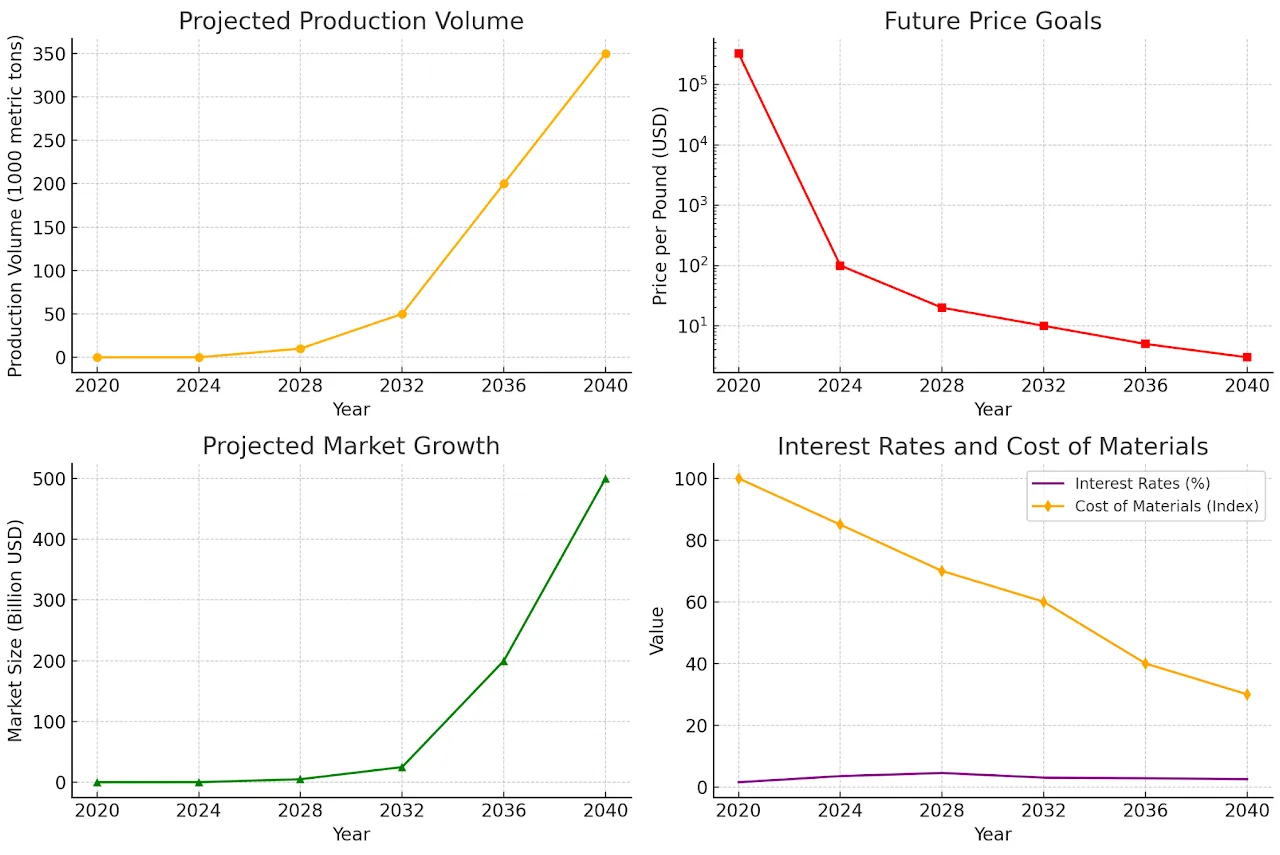

Trends in the cultivated meat industry from 2020 to 2040:

- Production Volume: Expected growth from near zero to hundreds of thousands of metric tons.

- Future Price Goals: Significant cost decline, approaching price parity with traditional meat.

- Market Growth: Projected revenue expansion from negligible to hundreds of billions of dollars.

- Interest Rates & Cost of Materials: Interest rates fluctuate while material costs decline, improving efficiency.

Image source: Author

Microeconomic Analysis of the Cultivated Meat Industry

Production Costs: CapEx, OpEx, and Cost-per-Kilogram Trends

Production costs are the central challenge for cultivated meat on a microeconomic level. Early prototypes were extraordinarily expensive, the first lab-grown burger (2013) famously cost around $330,000 to produce (C&EN). Since that 2013 prototype, the industry has achieved drastic cost reductions through R&D and scale-up, but costs remain high relative to conventional meat. Production costs can be broken down into capital expenditures (CapEx) for facilities and equipment and operational expenditures (OpEx) for running those facilities (including raw materials, labour, and utilities).

CapEx: Cultivated meat production requires sophisticated biomanufacturing facilities, essentially food-grade cell culture factories. Companies must invest in bioreactors (often steel tanks ranging from a few litres at lab scale to 10,000 litres or more at commercial scale), along with all the supporting infrastructure (sterilisation systems, sensors, HVAC for sterile rooms, etc.). Building even a pilot-scale plant is capital-intensive. For example, a small facility producing a few tons per year might cost tens of millions of dollars. A future large plant (e.g. 13,000 tons/year as planned by UPSIDE Foods) could cost on the order of hundreds of millions. These upfront investments mean high fixed costs, which drive up the cost per kg until the plant reaches high utilisation. Depreciation of this equipment and maintenance also factor into the cost per unit. At present, only a few companies (UPSIDE, Believer, Mosa Meat, etc.) are building pilot or demo plants, so industry-wide CapEx is in a ramp-up phase. Interestingly, we saw one major project adjustment: UPSIDE Foods put on hold its big Illinois plant plans in early 2023, partly to conserve cash and wait for clearer market signals (Leading Lab-Grown Meat Company Cuts Dozens of Jobs | WIRED). This illustrates that companies are cautious about over-investing in capacity until costs come down and demand is assured.

OpEx: Day-to-day operating costs are dominated by the cell culture media, the “nutrient broth” for cell growth. Studies indicate that media can account for 50 to 80% of total operating costs for cultivated meat (C&EN). This includes basal media components (amino acids, sugars, salts) and growth factors and hormones for stimulating cell growth. Initially, many of these ingredients were extremely costly (made for medical research). As noted, some growth media could run several hundred dollars per litre, which is untenable for food production. Companies have been actively developing cheaper media formulations and sourcing strategies. Thanks to these efforts, costs are trending downward. By late 2021, one of the leaders (Future Meat) reported its production cost for chicken had dropped to $7.70 per pound (~$17 per kg) (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year), and importantly, this cost was achieved largely by optimising media use and recycling (“media rejuvenation” technology) (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year). They managed to cut costs by over 50% in six months by improving how often they replace media and how efficiently cells use it (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year). This indicates that with biotech know-how, OpEx can be lowered significantly. Other OpEx components include energy (running stirrers, maintaining incubator temperatures), labour (skilled technicians to monitor batches), and quality control testing. As facilities automate and scale, labour cost per kg should decrease, but initially, it’s quite high because each batch might need careful, hands-on oversight by scientists. Energy efficiency will also improve with scale and better insulation/recovery systems, but companies are mindful that if their process uses a lot of electricity or steam, those utility costs add to each kilogram’s cost.

Cost per kilogram trends: Taken together, the trajectory is a steep decline, but starting from an extremely high point. From >$100,000 per kg a decade ago, some companies claim to be in the low hundreds of dollars per kg at pilot scale. For instance, Mosa Meat (NL) reportedly reduced its small-scale production cost to on the order of ~$100 per kg by around 2019 (from tens of thousands in prior years), and aims for further reductions. Future Meat’s achievement of ~$17/kg for chicken in 2021 is one of the lowest publicly reported figures (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year), and they projected getting near ~$10/kg with their next-gen facility. At $10/kg ($4.50/lb), they would be within a fewfold of conventional meat costs (for comparison, U.S. wholesale chicken in 2021 was ~$3.60/lb (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year)). Reaching that threshold would be a major milestone indeed, and Future Meat touted that $7.70 per pound is “getting closer” to parity, needing another ~50% drop (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year).

Microeconomically, as each company scales up production volume, economies of scale kick in: bulk purchasing of inputs, more efficient use of equipment, and spreading fixed costs over more units. Additionally, learning-curve effects (process improvements with experience) tend to trim costs with each successive batch. Looking ahead five years, industry experts and techno-economic analyses (TEAs) provide a range of cost projections. An influential TEA by Humbird (2020) suggested that in an optimistic large-scale scenario, the cost could come down to the ~$20 to $30 per kg range with current technology, remaining above commodity meat prices but much closer. More optimistic company roadmaps aim for <$10/kg in the late 2020s. For ground meat products (like minced beef or chicken nuggets), reaching single-digit dollars per kg might be slightly easier than for whole cuts that require more complex structuring. It’s worth noting that cultivated meat firms are also exploring hybrid products (mixing plant proteins with cultivated cells) to stretch the cultivated portion further and reduce cost per serving.

Production costs have fallen by orders of magnitude in a decade, and while they remain the biggest barrier, the trendline is favourable. Continued innovation in media formulation, cell line productivity, and process design will be critical to push cost-per-kg down to parity or below. Until parity is reached, high production costs mean high prices (or slim margins), which is why initial business models focus on low-volume, high-priced offerings.

Profitability Trends and Pricing Evolution

At present, profitability in the cultivated meat industry is virtually non-existent. Nearly all companies are in R&D or pre-commercial phases, meaning revenues (if any) are minimal compared to ongoing costs. The few companies that have sold products (GOOD Meat in Singapore, UPSIDE Foods, just beginning in the U.S.) are doing so in limited quantities, likely at a financial loss or, at best, breakeven when considering full costs. In this early period, companies rely on investment capital rather than operating profit to fund their activities. Negative profit margins are the norm, as is typical for a new tech industry scaling up (analogous to how early electric car makers or plant-based meat companies operated for years). However, tracking the trends and the path to future profitability is important.

Pricing evolution has been shaped by the need to balance exclusivity and consumer acceptance. Initial prices for cultivated meat dishes have been extremely high, positioned as a novelty or luxury experience. In the first commercial sale in Singapore (December 2020), a single serving of cultivated chicken nuggets was priced around $23 as part of a tasting menu (Today was the first commercial sale of cell-cultured meat in human …). In 2023 in the U.S., a high-end restaurant in San Francisco offered a cultivated chicken course (as part of a $150 tasting menu) and a restaurant in Washington D.C. sold a cultivated chicken entrée for about $70 (C&EN). These prices are orders of magnitude above equivalent conventional chicken dishes. They reflect the cost of production (which is very high per unit at this stage) as well as the experiential value and scarcity; essentially, a “first of its kind” markup. By contrast, in Singapore, GOOD Meat has tried to normalise pricing a bit: at Huber’s Bistro (a more casual setting), a cultivated chicken dish was priced under $15 (C&EN). While much pricier than normal chicken rice, $15 puts it in the range of an affordable luxury meal, suggesting the company is testing consumer willingness at different price points.

Over time, we expect prices to fall as production scales and costs decline. Companies may initially price above conventional meat to recoup R&D investments and because many consumers might pay a premium for the novelty or ethical aspects. Surveys indicate some segment of consumers is willing to pay more for cultivated meat (for reasons like animal welfare or environmental benefit). That said, widespread adoption likely requires near-parity pricing. Profitability will depend on achieving a cost of goods low enough that they can price competitively and cover overhead. At present, no company is profitable because volumes are tiny and costs high. But if a company can, for example, produce at $20/kg and sell at $40/kg (a high-end price, roughly $18/lb), there could be a margin to support the business, at least in fine-dining or gourmet retail channels. The trend in pricing thus far (from hundreds per pound down to tens per pound in pilot sales) is encouraging. GOOD Meat has hinted that as they expand in Singapore, they aim to price their product in line with premium organic meat. Another company, Wildtype (focused on cultivated salmon), has said its initial sushi-grade product will be expensive, but they plan to target price parity with wild-caught bluefin tuna (an extremely high-priced fish), effectively starting with the most expensive meat to make the comparison easier.

Profitability timelines vary by company. Some of the larger players have publicly suggested they could see commercial positive margins in the late 2020s if scale-up goes well. This assumes they can run larger facilities near capacity and that the per-unit cost comes down enough. In contrast, if technical challenges persist, many companies may not reach profitability without either charging very high prices or receiving subsidies. It’s possible that the first truly profitable cultivated meat businesses will be those that either (a) produce high-value speciality products (e.g., toro sushi, Wagyu beef slices), which command top dollar, or (b) supply ingredients (like cultivated fat or growth media components) to other food companies, which could have better margins initially than selling a pure meat product. Some firms are indeed looking at B2B ingredient sales (like cultivated fat to enhance plant-based meats) as a revenue stream.

In terms of price trends for consumers in the next 5 years: we are likely to move from ultra-premium pricing toward merely premium pricing. For example, by 2025 to 2026, one could imagine a cultivated chicken product in a grocery store at perhaps twice the price of free-range organic chicken. At that point, the product might appeal mostly to early adopters willing to pay more, but the gap would be much smaller than at present. As volumes increase, competition between producers could also drive prices down. Competition will prevent any one producer (when there are a few on the market) from keeping prices artificially high for long. Additionally, if traditional meat prices rise (due to supply issues or carbon taxes), the gap could narrow from both ends. It’s noteworthy that conventional meat itself is experiencing volatility during 2021; meat prices spiked due to supply chain issues (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year). Such spikes make alternatives relatively more attractive.

Profitability remains “only” a goal; no one is making money on cultivated meat, but through cost reductions and strategic pricing, companies aim to break even and to profit as they scale. We expect a gradual transition from novelty pricing to value-based pricing, with early profitable segments likely in high-end or ingredient markets. Achieving steady profits will require technical success alongside deft marketing and pricing strategy to align with consumer willingness to pay.

Cultivated Meat Industry Timeline (interactive embed by the author)

- 2013: First lab-grown burger produced at a cost of $330,000.

- 2020: First commercial sale in Singapore at $23 per serving.

- 2023: High-end U.S. restaurants offer cultivated meat dishes priced between $70 and $150.

- 2025: Projected premium market entry with prices approximately twice that of organic meat.

- 2030: Industry aims to achieve cost parity with conventional meat, targeting profitability.

The timeline illustrates key milestones in the development of the cultivated meat industry, from early scientific achievements to recent advancements in commercialisation and regulatory approvals.

Image Source: Author

Consumer Adoption Rates, Willingness to Pay, and Shifting Preferences

The ultimate success of cultivated meat hinges on consumer adoption. Will people eat it, and how do they feel about it? Over the past decade, awareness of cultivated meat was low but has been rising, especially after media coverage of milestones like the 2013 lab burger and recent restaurant debuts. Consumer surveys generally show a cautious optimism: a majority are at least curious to try it. According to a compilation of studies, more than 60% of consumers say they are willing to try cultivated meat, with only about 1 in 5 firmly unwilling (2022 Cultivated Meat State of the Industry Report). Notably, willingness to try is typically higher than willingness to buy regularly, which is to be expected for a new concept. Many people might taste it out of curiosity or novelty, but whether they integrate it into their diet depends on factors like taste, price, and perceived naturalness.

Demographics play a big role in adoption. Younger consumers (Millennials, Gen Z) tend to be more open to alternative foods. For example, one study cited in a Food Marketing Institute report found only 27% of Gen Z respondents were unwilling to try cultivated meat, versus 60% of Boomers unwilling (2022 Cultivated Meat State of the Industry Report). In other words, younger generations are much more willing to give it a shot, whereas a majority of older consumers reject the idea. Education and information also influence acceptance: surveys have found that when people are given a clear explanation of what cultivated meat is and why it’s being developed, acceptance rises significantly (2022 Cultivated Meat State of the Industry Report). Fear of the unknown can be addressed by familiarity as cultivated meat moves from an abstract concept (“lab-grown meat”) to a tangible product, which people can see and taste, consumer comfort is expected to grow. Early tasting events (often covered in the news) show generally positive reactions on taste, which helps build the narrative that “it’s real meat and it tastes like it.”

Willingness to pay is an interesting aspect. Because the product is so scarce, consumers haven’t really been tested on paying a retail price for it (apart from expensive restaurant meals). Survey data is mixed: some consumers say they’d pay a premium of, say, 10-20% more than conventional meat for a slaughter-free, eco-friendly alternative. Others indicate they’d only switch if the price is the same or lower. In practice, for analogous products like plant-based meats, we’ve seen that a small segment will pay more (e.g., many people buy Beyond Meat burgers at higher cost for ethical reasons), but mass adoption in supermarkets began only when those products approached price parity with meat or offered other value. We can expect a similar pattern: early adopters will pay a premium, but the broader market expects similar cost and quality.

As a result, companies are keenly interested in understanding how to market cultivated meat. Terms like “clean meat” were floated to emphasise environmental benefits, though “cultivated” or “cell-cultured” are more common labels. The naming itself may affect consumer perception (for instance, “lab-grown” sounds negative to some, so the industry avoids it). Regulatory-mandated labels (the USDA is leaning toward requiring the term “cell-cultured” on packages in the U.S.) will also influence how consumers view the product on shelves.

Consumer preferences are also shifting broadly in ways that favour cultivated meat’s value proposition. Over the past decade, there’s been a noticeable rise in flexitarian diets, with people trying to reduce meat consumption for health or ethical reasons without going fully vegetarian. These consumers might find cultivated meat attractive because it offers real meat without the guilt of animal slaughter. Additionally, high-profile concerns like antibiotic resistance, zoonotic diseases (bird flu, swine flu), and meat supply chain disruptions (as seen during COVID-19) have entered public consciousness. Cultivated meat can be positioned as a safer, more controlled alternative (no antibiotics needed, produced in sterile conditions). If marketed effectively, these points could sway health-conscious or safety-conscious consumers.

However, there are also perception challenges. Some consumers express an “ick factor”. The idea of meat grown in a bioreactor can sound unnatural or unappetising. Overcoming this will require education and positive experiences. The industry often draws parallels to fermentation (yeast making bread or beer in vats doesn’t bother people) or emphasises that the end product is biologically the same as meat. Transparency and education efforts are underway: companies give kitchen tours, show images of their farms without animals, and highlight the science in an accessible way.

In the next five years, as cultivated meat inches into the market, consumer adoption will likely start with small-scale tastings and limited releases. The number of people who have actually tried cultivated meat will grow from the lucky few hundred (to date) into perhaps tens of thousands when more restaurants and maybe speciality grocery offerings come online. This will help generate word-of-mouth and normalise the concept. We expect initial consumers to largely be sustainability-minded, tech-forward, or culinary adventurous individuals. Over time, if those people have good experiences, they become repeat customers and evangelists.

Consumer adoption is in its very early stages but with generally positive openness among the public, especially younger demographics. More than half of consumers surveyed are open to trying it (2022 Cultivated Meat State of the Industry Report), although a significant portion need convincing. Willingness to pay a premium exists in a niche but mass adoption will demand cost competitiveness. The coming years will involve carefully managing public perception, ensuring that early products taste great and are messaged correctly (safe, real meat, and beneficial). If successful, consumer preferences could indeed shift to incorporate cultivated meat as a normal part of protein choices, much as plant-based milks went from fringe to mainstream in a decade. But if early offerings disappoint or if misinformation spreads (e.g., unfounded safety scares), adoption could stagnate. At present, the industry is cautiously optimistic as consumer sentiment appears to be trending favourably, provided the value (taste, price, ethics) is clear.

Scalability Challenges: Infrastructure, Bioreactor Technology, and Bottlenecks

Scaling up cultivated meat production from laboratory petri dishes to industrial facilities is an enormous challenge that spans engineering, biology, and supply chain hurdles. While small-scale production (milligrams to kilograms) has been demonstrated by many startups, scaling to tens of thousands of kilograms (and beyond) is uncharted territory. There is “no playbook for biomanufacturing meat at scale” (Cultivated meat: ‘70-90% of players will fail in the next year’), companies are essentially writing the manual as they go, borrowing concepts from biotech but adapting them for food. Several key scalability challenges stand out:

Bioreactor scale-up: Growing cells in a 1-litre flask is very different from a 10,000-litre tank. As you increase volume, maintaining uniform conditions (nutrient distribution, oxygenation, temperature) gets harder. Cells are sensitive; if some areas in a tank have less oxygen or more waste buildup, cells there might die or not grow well. Stirring large volumes can also shear or damage cells. Thus, one challenge is designing bioreactors to keep cells happy at large scale. Traditional pharma fermenters (for CHO cells or yeast) can reach 10,000 to 20,000 litres, so in theory similar sizes are possible for meat cells. But most cultivated meat firms remain at pilot scale (a few hundred litres). In 2023, there was notable progress: around 10 new pilot or demonstration facilities opened worldwide (across Asia, Europe, North America) (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). By the end of 2023 there were reportedly 27 pilot-or-larger facilities planned or in operation globally (2022 Cultivated Meat State of the Industry Report). For instance, Mosa Meat opened a larger-scale plant in the Netherlands and CellX did so in China (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). These facilities are essential to identify scale-specific issues. A specific technical hurdle is achieving high cell density in large reactors; cell densities achieved might be on the order of 10^7 cells per mL; getting that higher means more meat output per run and lower cost. To boost yields, some companies use continuous or perfusion processes (constantly feeding in fresh media and removing waste) rather than simple batch processes (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year). Future Meat’s pilot plant used a perfusion “media rejuvenation” system to reach yields, which they claim are 10 times higher than industry standard (The Cost of Lab-Grown Chicken Dropped by More Than Half This Year).

Infrastructure and manufacturing scale: Even if the bioreactor tech works, building enough infrastructure is a massive task. To have a meaningful impact on meat supply, dozens of large facilities would be needed globally. Each facility is like a mini-refinery but for cells. Besides the tanks, you need sterile environments, large-scale media preparation and sterilisation units, harvesting and processing lines (to separate and form the cell biomass into meat products), and packaging lines. To prove the concept, most companies are building one pilot plant. The jump to commercial factory with thousands of tons output is likely a multi-year construction and commissioning process. Any delays in equipment delivery or construction (common in large projects) can bottleneck the scale-up timeline. We see long timelines: from announcement to first production, a plant might take 2 to 3 years. Additionally, these facilities require regulatory approval themselves (they must pass food-grade GMP standards, etc.), which is new territory for regulators and firms alike, possibly causing further delays. In the near term, limited production capacity is a bottleneck, even if consumer demand skyrocketed, the industry simply couldn’t supply volumes. It will take time to build infrastructure commensurate with mass demand.

Supply chain bottlenecks for inputs: As mentioned in macro supply chain, certain inputs like growth factors and specific media components are not produced at food-industry scale. If a company suddenly wanted to run a 10,000 L bioreactor continuously, the amount of growth factor needed might exceed global supply (since historically these were made in small batches for research). The industry may face shortages or long lead times for critical reagents until dedicated production ramps up. Some startups specialise in these inputs (for example, companies producing recombinant insulin or transferrin at large scale for cell ag). There’s also the challenge of cell line development: the cells used for cultivation need to be robust, fast-growing, and genetically stable. Creating and selecting cell lines for strong performance in large bioreactors is a bottleneck in itself. If cells senesce or slow down, yields drop. Firms often have to spend years isolating or engineering optimal cell strains for each species (chicken, beef, pork, etc.). Those biological R&D timelines can slow the overall scale-up if, say, the current cell line is fine for 500 mL but doesn’t thrive in 500 L.

Product formulation and downstream processing: Scaling involves more than growing cells; after growth, you have to process the biomass into a consumer-friendly product. For ground-meat type products (nuggets, burgers), this is somewhat straightforward: you can harvest cells (which may include muscle cells, fat cells, etc.), mix with seasoning or binders, and form patties or nuggets. Companies can use existing food processing equipment for grinding, mixing, etc. But for more complex products like steaks or whole cuts, scalability is tougher. These require scaffolds or structures, on which cells grow to form tissue. Making large, cheap, edible scaffolds suitable for big equipment is an active area of development. At present, a lot of whole-cut prototypes are small (a few centimetres) because that’s what can be done in small-scale scaffolds. To mass-produce something like a 250g cultivated steak, one might need a bioreactor with a scaffold network inside, plus a way to perfuse nutrients through it (like an artificial circulatory system). Scaling that kind of tech is a step beyond just cell suspension culture and is largely unsolved at industrial scale. So, many companies are initially sticking to simpler products that scale more easily (ground meat analogues or hybrid products).

Risk of batch failure and consistency: In scaling bioprocesses, one worries about contamination (a single bacterial or fungal contaminant can ruin a batch, which at large scale could mean thousands of litres of product lost) and consistency (each batch must meet food safety standards and have predictable nutrition profiles). Quality control at scale is non-trivial. To avoid contamination, companies will need rigorous testing and redundancy. This is similar to brewing or pharma, where contamination can stop production. Over time, moving to continuous processes might mitigate the batch stop/start issues, but that’s even more complex to manage initially.

Overall, these challenges make it clear why no one has produced cultivated meat at scale anywhere near conventional meat volumes. To illustrate, as of 2023 the largest annual production capacity in the world for cultivated meat is on the order of dozens of metric tons (C&EN), whereas conventional meat is 328 million tons in 2020 (C&EN). We are many orders of magnitude apart. Bridging that gap requires iterative progress: from pilot scale (hundreds of kilograms to a few tons), to demonstration scale (tens of tons), to commercial scale (hundreds or thousands of tons). Each step will reveal new issues. The next five years are pivotal; we’ll likely see the first commercial-scale plants come online by the late 2020s if things go well. Each success (or failure) will inform the industry. Importantly, capital and financing are linked to scalability: building large facilities and solving engineering problems requires a lot of capital. The recent funding crunch means some plans are delayed or scaled back. If capital remains tight, it could slow the pace of scale-up, as companies might not afford to build the infrastructure or hire the needed engineers. Conversely, a major technical breakthrough (say, someone achieves 10x cell density or super-cheap media) could attract a wave of funding and accelerate construction.

The industry faces a classic scale-up dilemma: proven in the lab, can it work in the factory? Bottlenecks include bioreactor design at large volumes, securing sufficient growth media and cell lines for scale, and building out costly production infrastructure. Progress is being made incrementally (new pilot plants and larger bioreactors are coming online, and early results are promising) but significant hurdles remain. The scalability question is perhaps the biggest uncertainty on the microeconomic side: it will determine unit costs, supply capacity, and ultimately whether cultivated meat can move from niche to mass market. Companies are racing to solve these issues, as whoever cracks the code of efficient large-scale production will have a major economic advantage in this budding industry.

Competitive Landscape, Major Players, and Market Consolidation

The cultivated meat sector started with just a few academic visionaries and startups, but in the last decade it has blossomed into a competitive landscape of over 150 companies spanning dozens of countries (2023 GFI Reports: Cultivated Meat and Fermentation Industries …). By 2023, there were 174 publicly announced cultivated meat companies worldwide (including those working on end products as well as those making inputs like growth media) (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). This includes startups focusing on a variety of species and products (beef, chicken, pork, fish, crustaceans, and even exotic meats) as well as enabling technology firms. The competitive field can be broadly categorised into: dedicated cultivated meat producers (companies whose main goal is to produce and sell cultivated meat products) and technology providers (companies specialising in scaffolds, cell lines, bioreactor tech, or media for the industry). At present, the industry is in a pre-revenue, R&D-heavy phase, so competition is more about technology and investor backing than about fighting for market share (since the “market” is extremely small). However, as companies approach commercial launches, the race to be first or best in certain categories is intensifying.

Major players (producers): A handful of startups have risen to prominence as leaders, often due to high-profile funding rounds, technical milestones, or public demonstrations. In the United States, UPSIDE Foods (renamed from Memphis Meats) is a front-runner backed by large investors (and even meat companies like Tyson and Cargill), it was among the first to showcase prototypes and is one of the first with U.S. regulatory approval for its product. Eat Just (GOOD Meat), while known for plant-based eggs, has a cultivated meat division that achieved the first sale in Singapore and also got U.S. approval; they focus on chicken and have served consumers in Singapore since 2020. Wildtype (cultivated salmon), BlueNalu (seafood), and Finless Foods (fish) are notable in the seafood segment, each developing cultivated fish products. In Europe, Mosa Meat (Netherlands) is famous for the first burger and continues to work on cultivated beef, while Meatable (Netherlands) is developing pork and beef with a focus on faster proliferation technology. Aleph Farms (Israel) is a leader in steak cultivation (whole-muscle cuts) and has the backing of some food giants; Israel in general is a hotspot with others like Believer Meats (renamed from Future Meat Technologies, focusing on chicken cost reduction) and SuperMeat. In Asia-Pacific, Shiok Meats (Singapore) is notable for shrimp and lobster, CellX (China) for pork/beef, and Upside Biotech (different from Upside Foods) in Japan. Each of these “major players” often has a different niche or species focus, which somewhat reduces direct competition in the very early stage.

Major players (inputs and tech): On the supply side, companies like Avant Meats focus on cultivation tech and have B2B aims, Exponent (renamed from PCulture) works on media formulations, and Matrix Meats or ECovative on scaffolds. These are part of the competitive landscape too, but more as collaborators or suppliers to the meat producers rather than head-to-head competitors.

Role of incumbents: Traditional food industry giants have been active. Several have made strategic moves: for example, JBS (world’s largest meatpacker) acquired BioTech Foods, a Spanish cultivated meat startup, in 2021 (2022 Cultivated Meat Executive Summary), and is investing $100M+ to build a production facility in Spain. Tyson Foods and Cargill invested in Upside Foods at an early stage, and Cargill also invested in Israel’s Aleph Farms. Nestlé, the world’s largest food company, has partnered to explore cultivated meat ingredients (they’ve worked with Israel’s Future Meat/Believer to potentially use cultivated beef in hybrid products) (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). Danone and other large food multinationals are also dipping in via partnerships or minority investments (2023 GFI Reports: Cultivated Meat and Fermentation Industries Growing Despite Drop in Investments: Cultivated X). This trend indicates that big players view cultivated meat as part of the future and prefer to have a foot in the door. It’s also a validation of the technology, but for startups, it means eventual competition from well-resourced corporations.

Competition dynamics: In the short run, competition is for talent, IP, and funding. With a limited pool of experts in tissue engineering for food, companies vie to hire the best scientists. They also race to patent innovations (as discussed below). We have seen some jostling in media for instance, one company might announce a cost breakthrough or a tasting event to claim leadership. However, explicit marketing competition for consumers is not really present, given the tiny market availability. Over the next 5 years, as products reach consumers in larger numbers, we’ll likely see competition heat up in specific product categories. For example, multiple companies aim to sell cultivated chicken in a given market like the U.S., who will secure the most restaurant partnerships or shelf space? Brand differentiation might become important (branding around purity, sustainability, taste, etc.). Companies may also compete on technology licensing; a smaller player with great tech might license to a bigger producer rather than compete directly.

Market consolidation trends: Given the large number of startups and the high costs involved, many analysts expect consolidation. We are seeing the early signs. Aside from JBS’s acquisition, UPSIDE Foods acquired Cultured Decadence (a lobster startup) in 2022, expanding into seafood products. This indicates bigger startups will swallow up niche ones to broaden their tech or product portfolio. Another form of consolidation is startups pivoting or shutting down if they can’t keep up with the funding downturn, it’s predicted that “70-90% of companies in this space are going to fail over the next year,” according to one early-stage investor (Cultivated meat: ‘70-90% of players will fail in the next year’). While that figure may be speculative, it underscores a common expectation: many of the 170+ companies will likely either merge, be acquired, or exit the market, leaving perhaps a few dozen serious players. We saw a similar pattern in the plant-based protein space (lots of entrants, followed by a shakeout where strongest brands remain). Consolidation can also take the form of partnerships: for instance, a cultivated meat startup might partner with a big meat processor to use their distribution network, effectively aligning rather than competing. Such partnerships (like Aleph Farms with Mitsubishi in Japan (As Japan commits to cultivated meat, will Europe be left behind?)) can blur competitive lines and create coalitions aimed at different regions.

Another trend is specialisation vs. diversification: some companies double down on a speciality (e.g., one species or one part of the value chain), while others expand. The competitive landscape will likely feature a few “full-stack” companies, which do everything from cell line to production to marketing of their own branded product, and a host of specialised firms feeding into the ecosystem. Those specialised firms might get acquired if their technology is critical, for example, a company with a superior growth medium might be bought by a bigger cultivated meat firm to secure that advantage exclusively. At present, the major players appear to be the ones with strong funding and technical milestones, and they hail from the U.S., Europe, and Israel primarily. But watch Asia: China’s startups (with backing) could quickly become major contenders, especially in pork (the largest meat market). Likewise, Japan, South Korea, and others are nurturing domestic players. We could see new “major players” emerge from those countries in the coming years, altering the competitive map.

In terms of market share, since sales are minimal, it’s more useful to look at share of investment as a proxy: a large portion of all funds raised has gone to the top 5-10 companies (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology). In 2023, the top five cultivated meat companies accounted for about 47% of all funds raised historically, indicating a concentration of resources among leaders (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology). This financial power often translates to a head start in scale and market entry. If that continues, those leaders will likely capture outsized market share when sales ramp up, potentially leaving smaller players to either find niche markets or be acquired.

Competition with other alternatives: An often-ignored aspect is that cultivated meat competes with conventional meat and, indirectly, with plant-based proteins and fermentation-based alternatives for the “ethical eater” market. For example, a consumer wanting to reduce meat might choose between a plant-based burger, a mushroom-based meat alternative, or cultivated meat. So cultivated meat companies are also watching the plant-based industry’s ups and downs. The recent plateau in plant-based meat sales has made some investors wary of all meat alternatives (Cultivated meat: ‘70-90% of players will fail in the next year’). Cultivated meat firms have to differentiate their product (it’s real animal meat, just grown differently) to avoid being lumped into the same category if plant-based hype continues to wane.

The competitive landscape is crowded but in flux. We have a growing roster of startups, a few clear front-runners by funding and technical progress, and an increasing presence of incumbent food companies via investments or acquisitions. The next few years will likely bring a shakeout. Many startups may consolidate or exit, while the winners emerging from this phase will set themselves up as the first major brands of cultivated meat. This consolidation is a natural part of industry maturation, especially given current economic pressures. Companies able to demonstrate real progress (scaling tech, reducing costs, obtaining regulatory approvals) will survive and likely absorb others. Those that cannot will struggle to raise funds and might fold. Thus, from a microeconomic perspective, competitive forces will drive the industry toward a smaller number of viable players, each hopefully operating at larger scale, by the end of the decade.

Patent Activity and Research Trajectories

The cultivated meat sector is as much a scientific endeavour as an entrepreneurial one, and we’ve seen a surge in research output and patent filings accompanying its rise. In the early 2010s, research on cultured meat was sparse. Only a few academic labs (e.g., Maastricht University with Mark Post, and some tissue engineering groups) were published on the topic. Over the past 10 years, however, interest from academia, industry R&D, and government research programmes has grown exponentially. This can be gauged by the number of scientific publications, dedicated conferences, and the establishment of research centres (such as Tufts University’s Center for Cellular Agriculture in the U.S., or research consortia in Europe).

On the patent front, companies and universities have been racing to protect intellectual property related to cultivated meat. Key areas of innovation include: cell line development (creating stable, high-yield cell strains), cell culture media formulations, bioreactor designs and processes, scaffold materials and structures, and end-product texture/flavour processes. According to patent data analyses, there was an “almost four-fold increase” in patent filings for cultivated meat from 2019 to 2020, followed by a further ~20% increase in 2021 (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology). This reflects how, as investment money flooded in around 2018 to 2020, R&D efforts ramped up and companies moved to secure IP. By 2022, patent filing growth slowed to a modest 3% uptick (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology), possibly due to a combination of the patent landscape maturing and the funding slowdown that year (less money to spend on patenting every idea). Nonetheless, the overall trajectory is a dramatic rise in accumulated patents compared to a decade ago. GFI Europe noted that in the alternative protein space broadly, European alternative protein patents increased 960% in a decade, and within that, cultivated meat is a fast-growing segment (European Alternative Protein Patents Increase by 960% in a Decade).

A report by IP firm Appleyard Lees highlighted that global investment trends correlate with patent trends: the dip in filings in 2022 coincided with investor cooling (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology) (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology). It also pointed out that as of 2023, the top companies by funding hold a significant chunk of the patents, which could create barriers for newcomers (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology). For example, Upside Foods, Eat Just, and others have built IP portfolios around their specific methods (Upside, for instance, has patents on certain serum-free media techniques, and Aleph Farms on thin-cut steak cultivation methods, etc.). However, since the field is new, there isn’t an “IP monopoly”. Multiple groups around the world are finding different approaches to similar problems, and many patents are likely overlapping or will need cross-licensing.

On the research side (academia and open science), there has also been significant progress. Government grants and public research initiatives have increased. The EU funded a programme called “Meat4All” in 2020, and national science foundations in countries like the U.S., Netherlands, Israel, Japan, and Singapore have issued grants for cultivated meat research. Open-access research has been encouraged by organisations like the Good Food Institute, which has sponsored academic work and even released open-source cell lines. For instance, GFI and partners have developed some publicly available cell lines for pork and beef to help new startups or researchers who might otherwise spend a long time isolating cells. This open science approach is meant to spur innovation across the board, including at less-funded players. Key research trajectories include improving cell growth rates, optimising media (perhaps using plant hydrolysates or other cheaper ingredients), finding edible scaffold materials (such as textured plant proteins, mushroom mycelium scaffolds, or 3D-printed edible polymers) to support cell growth into muscle-like structures, and improving the end-product’s sensory attributes (flavour, aroma, and how it cooks). There’s also research into the nutrition profile, e.g., can cultivated meat’s fat content be manipulated to be healthier (like more omega-3 fatty acids) or could micronutrients be added? Patents have been filed on some of these ideas too (for example, upside or others might patent a method to co-culture muscle and fat cells to get the right fat marbling). Another area of patents is bioprocess hardware: companies have filed patents on novel bioreactor designs specific to meat (some designs incorporate scaffolds inside, some use carrier beads for cells, etc.), or on methods to continuously harvest cell biomass.

One interesting note: because this industry is so new, there’s been an effort to avoid a thicket of patents with the potential to stifle progress. Some key early patent holders (like academics) have been collaborative. However, as money flows, the patent race is inevitable. By one count, hundreds of patent applications related to cultured meat have been filed worldwide, and the growth from 2016 onward is steep (2022 Cultivated Meat Executive Summary). In China, domestic patent filings in cell ag have also increased since it became part of the national plan. China could become a big source of patents in the area, potentially creating a separate sphere of IP.

It’s also worth mentioning patent expirations and public domain tech: A very early patent for cultured meat production was filed by Willem van Eelen and others around 1999 to 2001 (often cited as the first cultured meat patent). Those patents (if maintained) would be expiring around this time, which might free up some basic ideas. New patents are more specific. For example, a company might patent a growth medium that replaces certain amino acids with cheaper sources or a specific gene edit that makes cells grow faster. As the industry matures, there might be patent disputes or the need for licensing deals, especially if one company’s breakthrough is needed by others. This could shape the competitive landscape; e.g., if Company A holds a crucial media patent, Company B might have to license it or develop a workaround.

From a microeconomic perspective, the increase in patents and research is a good proxy for innovation and technological advancement, which in turn drive cost reductions and product improvements. The plateauing of patent growth in 2022 (Patent data shows innovation in the plant-based meat remains historically high: Food and Drink Technology) might hint that the easiest, broad concepts have been patented and that deeper, incremental innovations are being pursued. It might also reflect a bit of caution as firms focus on commercialisation rather than filing patents for every idea.

Research trajectories are on a steep upward climb, and scientific understanding and technical capabilities are improving every year. The field has progressed from “can we grow a piece of muscle at all?” to “how do we efficiently produce tons of meat that tastes great?”. Patent activity mirrors this, with a burst in filings as companies stake claims on their inventions. Even though there was a slight slowdown in 2022, innovation remains high. We can expect continued growth in publications and patents, though perhaps more targeted and practical as the industry shifts from purely R&D to scaling up. The interplay of open research and proprietary IP will be important: too much secrecy could slow collective progress, while a collaborative approach (with shared foundational knowledge) could help everyone innovate faster. To date, the trend indicates a vibrant and growing knowledge base that should push the industry closer to its goals.

Consumer Adoption of Cultivated Meat (interactive embed by the author)

Overall Adoption

Response Share Willing to Try 60% Firmly Unwilling 20% Undecided 20% Unwillingness by Generation

Generation Percentage Unwilling Gen Z 27% Boomers 60%

Forecasting the Next 5 Years: Industry Outlook and Economic Modelling

Market Expansion Scenarios and Growth Modelling

Projecting the next five years (2025 to 2030) for cultivated meat involves significant uncertainty, but we can sketch scenarios to understand possible paths. Broadly, scenarios range from optimistic (rapid expansion) to conservative (slower, steady progress), with inflection triggers making the difference.

High-Growth Scenario: In this case, technical and regulatory hurdles are overcome relatively quickly. Drivers would include one or two companies achieving a major cost breakthrough (e.g., media costs plummet, or a 20,000-litre bioreactor runs successfully), and major markets opening up (EU approval by ~2025, China by ~2027). With those, the industry could scale production faster than current expectations. We might see dozens of restaurants and speciality retailers offering cultivated meat by 2026, and perhaps the first entrance into mainstream grocery stores by 2028 in some regions. Quantitatively, the global cultivated meat supply could grow from essentially <100 tons in 2024 to a few thousand tons by 2027, and perhaps 10,000+ tons by 2030. This would remain tiny compared to conventional meat, but it represents an annual growth rate in the high double or even triple digits for a few years. In revenue terms, if prices also fall, the industry could be on track to hit several billion dollars in sales by 2030 (for instance, 10,000 tons at an average price of $20/kg would be $200 million; scale that to 100,000 tons and ~$10/kg average by 2030 for $1 billion revenue not implausible if multiple large facilities come online late in the decade). Market share would remain small, but investor confidence in this scenario would be high, potentially unlocking even more capital. This scenario aligns with forecasts like McKinsey’s $25 billion by 2030 (Cultivated meat: Out of the lab, into the frying pan | McKinsey) and AT Kearney’s notion of ~1/3 of meat supply from alternatives within 10 years (though their timeline seems very aggressive) (AT Kearney expects alternative meats to make up 60% market in 2040: The Futures Centre). We would see perhaps a consolidation around a few big players who manage to scale those companies would have the lion’s share of that output.